Let’s be honest — budgeting doesn’t sound like the most fun thing in the world. But it’s a game-changer for your finances once you get used to it!

A monthly budget not only keeps you organized, it can also help you save more money and pay off debt more quickly.

In this guide, I’ll show you how to create a monthly budget that works for you, share some tips for success, and explain how Lunch Money makes the process a piece of cake!

Why is budgeting important?

Budgeting lets you decide exactly where your money should go — whether toward bills, savings, debt, or something fun.

Does this sound familiar?

Your paycheck hits your bank account — you pay your bills, buy groceries, and maybe treat yourself to a night out.

But within a week or so, you find yourself low on funds again, waiting for the next payday.

It feels like there’s never enough leftover for savings or to pay down debt. And fingers crossed, no surprise expenses like an emergency car repair pop up.

If this sounds familiar, you’ll likely benefit from a simple monthly budget. Once you know the important stuff is covered, you can splurge on whatever makes you happy without feeling guilty.

How to make a monthly budget (step-by-step guide)

If you’ve never budgeted before, it can initially feel pretty overwhelming.

But don’t stress too much…it’s pretty simple! And we’re here to walk you through each step!

1. Choose a budgeting method

Your first step is to choose a budgeting method. There are several ways to budget, each with pros and cons. You’ll need to choose a budget that works for you. Here’s a closer look at a few common budgeting types:

- 50/30/20: The 50/30/20 budget is a simple method that requires you to split your income three ways — 50% to needs, 30% to wants, and 20% to savings or extra debt payments. It’s an easy way to budget, but you may need to adjust the ratios depending on your lifestyle.

- Zero-based budgeting (ZBB): With a ZBB budget, you assign every dollar a job, aiming to have zero dollars remaining after subtracting your expenses from your income. It’s a hands-on approach that ensures every dollar is accounted for and nothing goes to waste.

- Envelope method (Cash Stuffing): Similar to a zero-based budget, you assign a job to each dollar you earn. But while a true envelope budgeter would divide cash for each category into physical envelopes, you can emulate the process virtually with apps like Lunch Money.

It’s okay to experiment with different methods to find the best one for you.

2. Calculate your monthly income

You may already know your monthly income. If not, check your paystubs and/or bank account. Either way, tally up all your income sources to determine how much money you have to work with for your budget.

Make sure you include your employment income, along with any side hustle earnings, government benefits, family assistance, etc.

Add them up, and you will have your total monthly income!

Pro tip: Some people’s income changes from month to month. They might be self-employed, earn a commission, or work fluctuating hours. This can make budgeting more challenging. If that’s you, try using your lowest-earning month (over the past several months) as the baseline for your budget. You can always make adjustments later.

3. Create your expense categories

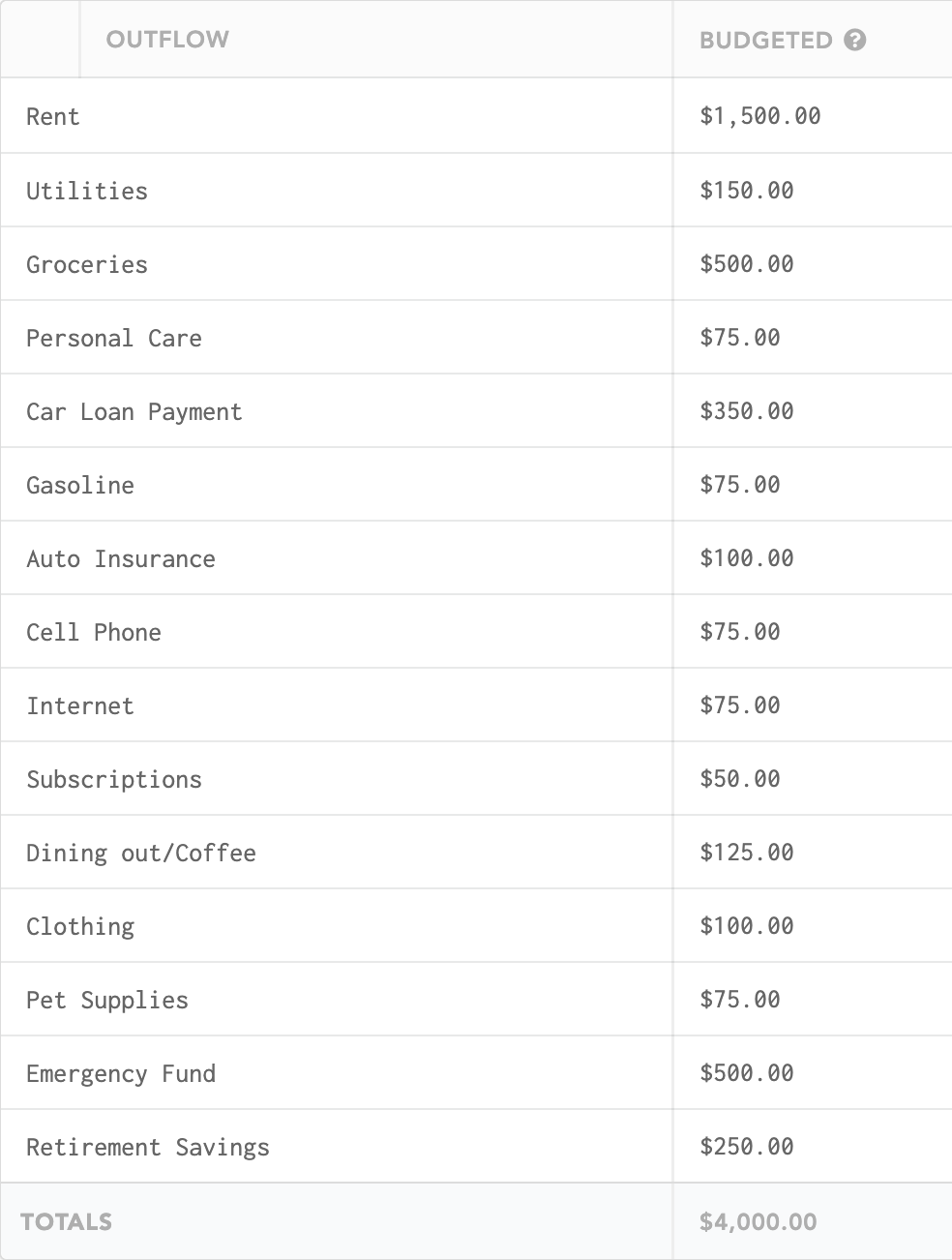

Once you’ve determined your monthly income, it’s time to create your various expense categories and assign a projected spending amount to each category. Here is a basic budget example that illustrates what this might look like for someone budgeting a $4,000 monthly income:

If this is your first time budgeting, you might not know how much you spend in specific categories, such as groceries, gas for your car, or dining out. One way to get a handle on this is by reviewing the individual expenses from the past few months’ bank or credit card statements. You can connect to your bank through Lunch Money to easily and automatically retrieve all your historic transactions!

This will give you a rough idea based on your typical spending.

4. Calculate your bottom line

Subtract your expenses from your income to ensure you have enough money to cover your costs. Depending on your chosen budgeting method, you can allocate extra funds toward savings, paying down debt, or rolling it over into next month’s budget.

5. Track your expenses throughout the month

While it’d be nice just to make a budget and go on your merry way, keeping up with your transactions throughout the month is critical. Skipping this step could lead to overspending, especially in discretionary areas like restaurants and shopping.

This doesn’t have to be complicated, though! Budgeting tools, like Lunch Money, automatically track and categorize your transactions for you.

6. Make next month’s budget

You completed your first budget — congratulations! Now, it’s time to prepare for next month.

First, review each expense category from your last budget. Did you spend more than what you allocated? Did you spend less? Why?

Use these insights to make adjustments for your next budget. Don’t forget to include any upcoming expenses like birthdays, car maintenance, or subscription renewals.

8 tips for creating a successful budget

-

Set clear goals: Goals give you something to work toward. Try setting S.M.A.R.T. goals (Specific, Measurable, Achievable, Relevant, and Timely.) For example, saving $5,000 for an emergency fund within 12 months.

-

Use a budgeting app: You can track your finances on paper or with a spreadsheet, but it’s a tedious process that can be hard to keep up. Budgeting apps like Lunch Money save you time by automatically tracking and categorizing your transactions, and taking care of the math for you.

-

Know the difference between needs and wants: When you really want something, it’s easy to believe you need it. Take time to reflect on what you truly can’t live without.

-

Automate your savings: Have you ever heard the term “pay yourself first”? Before touching your paycheck, set aside a portion for savings (automatic transfers make this easy).

-

Build an emergency fund: Unexpected expenses, such as car repairs or medical bills, can happen anytime. Without a financial safety net, emergencies can derail your budget and may even require you to take on debt.

-

Plan for irregular expenses: We all have those weird expenses that appear once a year or maybe once a quarter. Set aside money each month to prepare for these and factor them into that month’s budget.

-

Celebrate the small wins: When you reach a goal, find a way to celebrate (within reason). Take a day off, treat yourself to takeout, or buy that cozy sweater you’ve had your eye on.

-

Be flexible: Your budget isn’t set in stone. Expenses (and income) can vary from month to month. Don’t be afraid to adjust wherever needed.

How Lunch Money supports monthly budgeting

Budgeting apps make it much easier to view your income, plan for expenses, and monitor spending habits.

And we’re not just being biased when we say that Lunch Money is one of the best budget planners around. Okay, we’re maybe just a little biased.

Here are just a few of its awesome features:

-

Automatic account syncing: Add your bank and credit card accounts to Lunch Money. Not only will you be able to view all of your transactions in one place, but Lunch Money will pull them from your bank automatically, making the process effortless.

-

Unlimited categories and category groups: With Lunch Money, there’s no limit to how many budget categories you can make. You can even align similar categories under category groups.

-

Multi-currency support: Lunch Money supports multiple currencies, including dollars, euros, and yen. This allows frequent travelers or digital nomads to track expenses in multiple expenses while seeing how it all adds up in your chosen currency. You can also view your crypto holdings in the same currency as your traditional investments.

-

Custom budgeting periods: Lunch Money lets you choose custom budgeting periods that start on any day of the week. We’ve got you covered whether you want to budget weekly, bi-weekly, or monthly, something no major budgeting app does.

-

Collaboration feature for couples: If you have a spouse or partner and prefer to budget as a couple, you can each have a Lunch Money login and password and modify the budget, categorize transactions, and view reports.

-

Different budgeting methods (50/30/20, zero-based, envelope): Remember how we mentioned budgeting methods earlier? Well, Lunch Money supports them all!

Monthly vs. bi-weekly budgeting: Which is better?

Deciding whether to budget monthly or bi-weekly comes down to personal preference.

Monthly budgeting is very common, perhaps because many fixed expenses are billed once per month. It provides a complete picture of your monthly income and expenses, allowing you to plan for them more easily.

However, if you get paid every other week, you may find it’s more practical to budget bi-weekly.

Each payday, you can adjust your spending based on what you’ll need to cover your expenses, savings, and debt for the next two weeks.

The downside of a biweekly budget is that it requires more time and effort to maintain. That said, looking at your finances more often may help you avoid overspending.

If you’re unsure which method to choose, try experimenting with both to see which works best for you!

Summary

A monthly budget lets you see exactly where your money is going so you can hit your savings goals and tackle your debt.

While there are a lot of good apps out there, Lunch Money is one of the most flexible. Between its custom budget categories, unlimited categories, automatic account syncing, and multicurrency support, the app makes it easy to create a budget and track your progress.

Sign up today for our free 30-day trial (no credit card required) to see how we can improve your finances!