The 50/30/20 rule is a straightforward budgeting method that divides your net income into three categories: needs, wants, and savings. The idea is to allocate 50% of your income on needs, 30% on wants, and 20% on savings. The method works well for those who prefer a simple approach to budgeting and don’t want to track every transaction.

Let’s break down the different categories!

Needs

Needs are expenses you must pay to live, such as housing, food, clothing, and transportation. It also includes minimum payments on any debts.

It can be easy to misinterpret wants as needs. For example, you need clothing, but you don’t need designer clothes. You can likely buy items at thrift stores. However, you may need steel-toe boots for work or a coat for the winter. It’s important to be honest when determining if a purchase is a want or need.

Wants

Wants are considered items that improve our quality of life but that we don’t need to live. They are often referred to as non-essentials or discretionary expenses. Examples include money spent on a warm vacation, tickets to a football game, or dining out at restaurants.

Savings

Savings are any funds you set aside to better your future. This can include money that you put into a savings or retirement account. However, you can also allocate debt payments over and above the minimum payment in the savings category.

Also, don’t forget about any retirement plans at work. For example, anything you or your employer contribute to your 401(k) also counts.

What if your ratios are off?

After categorizing your expenses, you may find that your ratios don’t align with the 50/30/20 budget. This is often the case for those living in a high-cost area and spending half their income on housing alone.

If your needs take up more than 50% of your income, consider whether you can reduce any expenses or work towards lowering them.

Minimum debt payments can also push the needs category up over 50%. If so, we recommend creating a plan to pay down your debts.

Ultimately, you may have to adjust your ratios while you work to make changes, and that’s okay! Perhaps a 60/20/20 or 70/20/10 split is the best you can do right now. Accepting where you are and knowing that changes take time is important. You aren’t doing anything wrong because your budget doesn’t immediately fall into the recommended ratio; keep them in mind and slowly work towards optimizing your finances.

Sample 50/30/20 budget

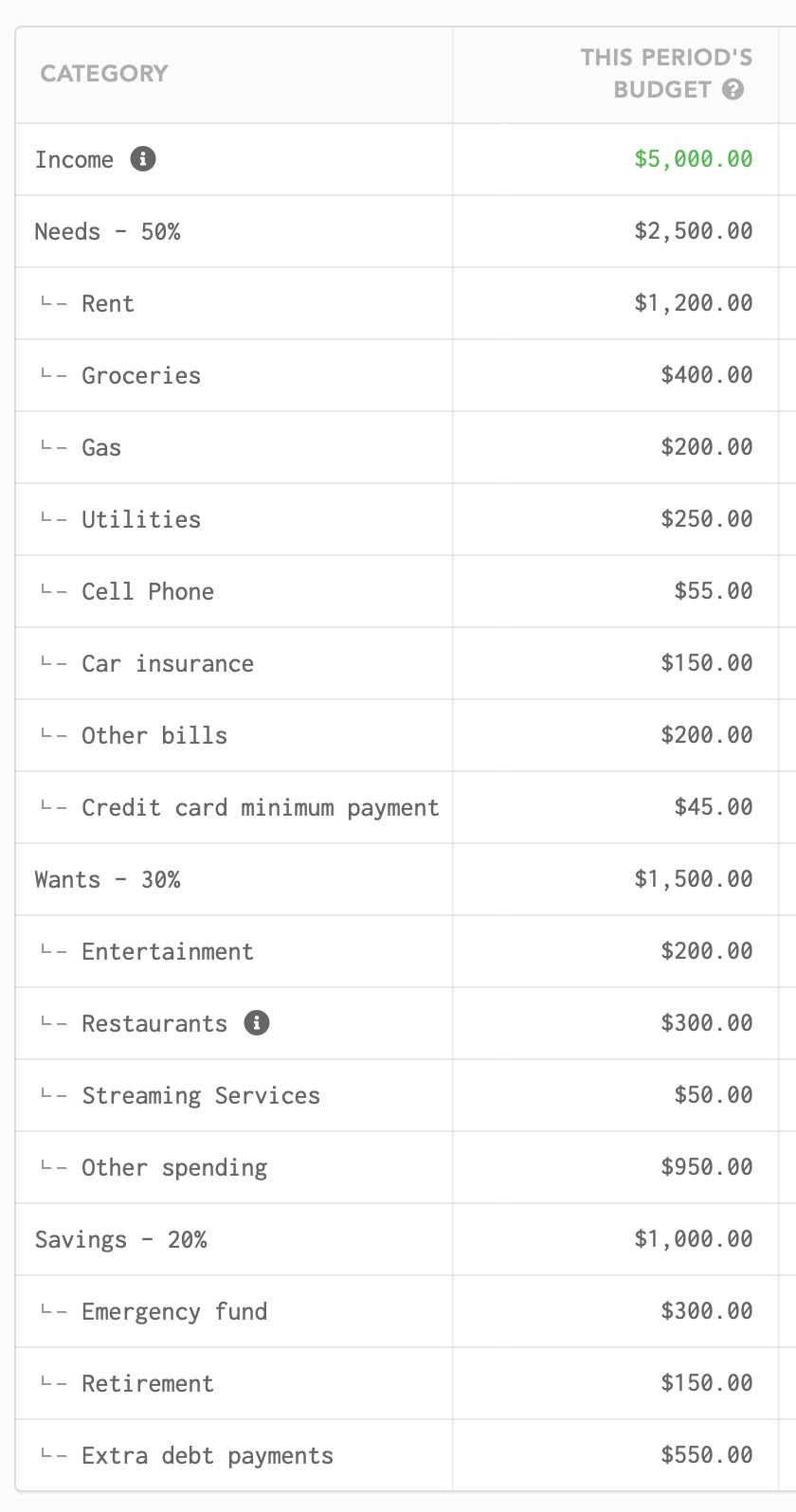

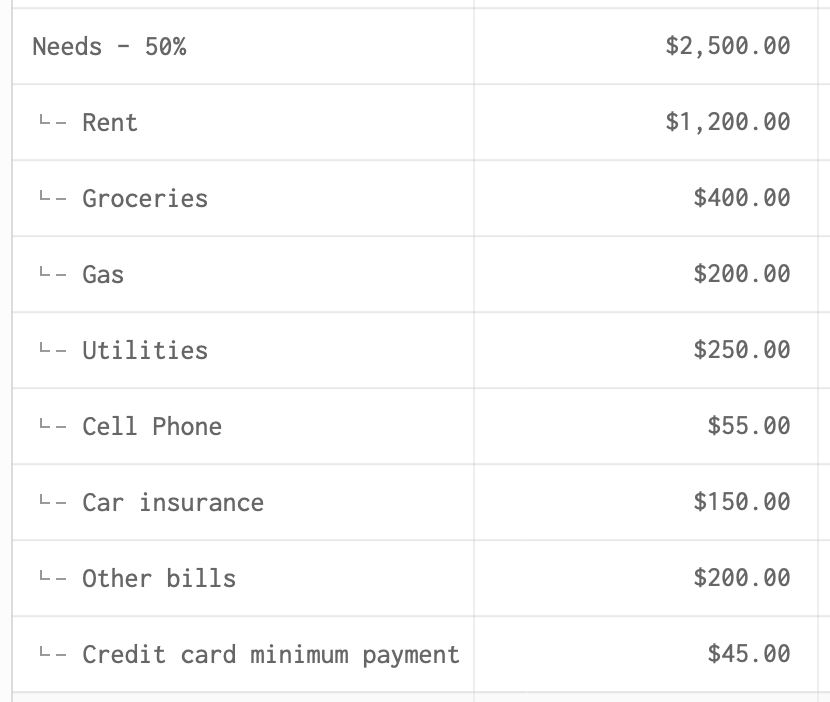

Let’s make a sample budget for someone who brings home $5,000 per month. That would leave $2,500 for needs, $1,500 for wants, and $1,000 for savings.

It might look something like this:

How to use the 50/30/20 budgeting method in Lunch Money

Did you know? You can follow a 50/30/20 budget with Lunch Money using budget categories and category groups.

Categories are for individual line items, such as “groceries” or “car payment.” Category groups are, well, groups of categories. The screenshot below shows that “Needs - 50%” is a category group. Below that are the individual categories.

On the “Needs - 50%” line, you can also view the total budget for the group: $2,500.

As you change the budgets of the categories in the group, the category group total will update automatically. This makes it easy to see exactly where you stand for each section. It’s also easy to move categories from one group to another.

50/30/20 rule alternatives

Of course, the 50/30/20 budget isn’t for everyone. Here are a few other budgeting methods to consider:

Envelope budget method (cash stuffing)

In its truest sense, envelope budgeting requires you to divide actual cash into labeled envelopes that represent your various budget categories. For example, when you receive your paycheck, you would take cash and put money into a “groceries” envelope, a “gas” envelope, etc. Then, when you go grocery shopping, you spend directly out of the “groceries” envelope.

However, in today’s digital world, you can do this virtually using a spreadsheet or budgeting app like Lunch Money. You set spending categories that are funded when you get paid. Then, your transactions are allocated to the appropriate category.

Zero-Based budgeting

Zero-based budgeting is a hands-on approach that requires you to assign every single dollar of income into a category. With this method, you decide ahead of time what you will do with each dollar. If you overspend in one category, you must remove some budgeted funds from another category to cover it.

Some people create a “buffer” category they can pull from if they go over budget in another category.

Pay Yourself First budgeting

The pay-yourself-first budgeting method might be the simplest out there. Your first step is to decide how much of your income you want to save and have the amount automatically transferred to savings. This is considered “paying yourself first.” From there, you are free to spend the rest of your discretionary income knowing you are meeting your savings goals.

This works well if you have plenty of additional cash flow and can easily save enough to meet your goals. Otherwise, you may need a budget with more built-in accountability.

Who is the 50/30/20 budgeting rule best suited for?

The 50/30/20 budget is ideal for those who don’t want to track every transaction. This allows for broader categories and less tedious tracking.

For example, you could have a category just for “wants” and budget 30% of your take-home pay into that category. Then, you don’t have to worry exactly how much you spend in individual categories, as long as your overall spending on your wants is 30% or less of your take-home pay.

Some people will even set up a separate checking account for this purpose. They know they can spend freely from that account because their needs and savings are covered.

FAQs

Is the 50/30/20 budgeting rule still valid?

If your income aligns with the cost of living in your area, then the 50/30/20 budget could work for you. However, those living in a high-cost-of-living area or with high minimum payments on their debts may struggle to keep their expenses within the 50/30/20 ratio.

Is saving 20% of your income realistic?

According to T. Rowe Price, saving 15% towards retirement is appropriate for many, but you must also remember to save for emergencies and other financial goals. Therefore, saving 20% isn’t an extraordinary amount.

Increasing your income is your best bet if you struggle to meet this goal. You can do this by starting a side hustle or getting a raise at work. From there, direct your extra income towards saving or paying down debts.

What is an example of a 50/30/20 budget?

A family following a 50/30/20 budget bringing home $6,000 per month would allocate $3,000 towards needs, $1,800 to wants, and aim to save $1,200 per month.