With the pay-yourself-first budgeting strategy, also known as reverse budgeting, you determine what you want to save first and then allocate the rest of your funds for your day-to-day living. As long as you are meeting your savings goals, how you spend your money otherwise isn’t as important.

What Does Pay Yourself Mean?

By paying yourself first, you prioritize savings over spending. Once that’s done, you can spend your remaining money however you like. It guarantees that you will always meet your savings goals and that if you run short, your discretionary spending will take the hit instead of your savings.

People often take the opposite approach to budgeting by deciding how to spend their money and then just saving what is left over. But this makes savings an afterthought and can lead to overspending and unachieved goals.

Reverse Budget Example

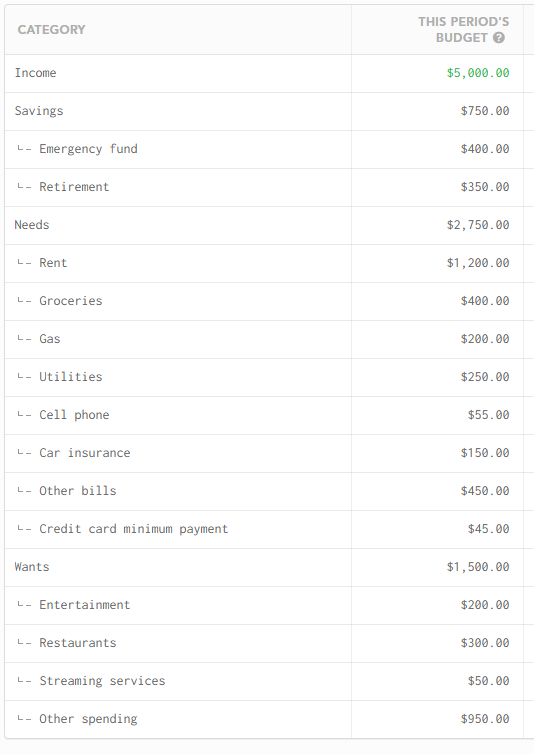

Let’s say you bring home $5,000 per month and want to save 15% of your income. That would mean you’d need to save $750 per month. You might split that up to save $400 for retirement and $350 into your emergency fund.

That leaves you $4,250 to spend on your needs and wants. If you’re budgeting with Lunch Money, it might look something like this:

So, if you get paid twice a month, you’ll transfer $375 from each paycheck to savings and live on the remainder.

Tips for Implementing a Reverse Budget

Here are a few ways you can implement a reverse budget.

Split direct deposit: If you know how much you want to save from each paycheck, you can ask your HR department to split your direct deposit and send that money directly to your savings account. This way, you won’t ever see the money in your checking, thus reducing the temptation to spend it.

Contribute to your 401(k): Another way of saving without ever seeing the money is to contribute to your 401(k). This can be doubly helpful if your company matches a portion of your contributions, making this form of savings extra powerful.

Automatic transfers: Automatic transfers also work well with pay-yourself-first budgeting. You can instruct your bank to send a regular amount from your checking to your savings account. If you want to transfer funds to an IRA, you can set up automatic investments with the broker that houses your investments.

Does Lunch Money Support a Pay Yourself First Budgeting Strategy?

Lunch Money’s budgeting tool supports a pay-yourself-first approach by allowing you to create detailed budget categories, which can roll up to category groups. For example, you could create an overall “Savings” category group that breaks out into individual categories, such as “high-interest savings account,” “401(k)”, “IRA,” etc.

Of course, the key to successful budgeting lies in the execution, which is why it’s so important to set up automatic transfers to your savings account as soon as you get paid.

Reverse Budgeting Pros and Cons

Pros

- Consistently meet your savings goals: The end goal of any budgeting system is to ensure that your savings goals are met. Paying yourself first guarantees that you always save the amount you intend.

- Suitable for long-term security: If your retirement contributions go to your retirement savings account automatically, you can’t accidentally spend that money, and your long-term retirement goals will be funded.

- Keeps overspending to a minimum: If you have a habit of spending money simply because you have it, paying yourself first will curb some of your overspending. Once your savings goals are met, you can spend whatever is left over.

Cons

- Less flexible than other budgeting methods: Paying yourself first is less flexible because you transfer money to savings as soon as you receive it, making that money unavailable if something comes up.

- Saving too much: This might seem impossible. After all, how can someone save too much? But if you transfer too much to savings, you may need to withdraw often to cover expenses, undoing your progress. This can be demoralizing, and you may feel there is no point in trying to save.

- Not fully considering debt: If you have debt, you’ll likely want to focus on paying off your loans before growing your savings. Also, if you are taking on debt because you are putting too much into savings, you are digging a financial hole that you may have been able to avoid.

Who Should Use a Reverse Budget Strategy

The reverse budget strategy could be helpful for natural spenders, budget haters, and fans of 50/30/20 budgeting.

Natural spenders: If you make spending decisions based on how much money is in your checking account, you could easily spend money that could have been saved. Following a pay-yourself-first strategy and moving money directly into savings removes the temptation to spend it.

Budget haters: If you hate tracking your spending in a budget, paying yourself first might be the perfect budgeting strategy. It ensures your goals are met, and you can spend the rest of your money without worry. You don’t need to track your spending if you save enough for retirement, emergencies, and larger purchases.

However, if you have trouble getting through the month without using debt or withdrawing from savings, you may have to consider a different budgeting method.

50/30/20 budgeters: The 50/30/20 budget allocates a percentage of income for savings. It calls for spending 50% on needs, 30% on wants, and saving 20%. If you’ve implemented this system, even if your percentages are exactly 50/30/20, then transferring your savings into the appropriate account as soon as it arrives could be useful.

Those with a higher income or lower expenses: If you are easily covering your monthly expenses, paying yourself first can make a lot of sense.

Who Should Not Use a Reverse Budgeting Strategy

Reverse budgeting is difficult to implement if you don’t have a lot of discretionary income. If you regularly struggle to make it to your next paycheck, paying yourself first might not be the ideal budgeting tool. You may transfer money to savings simply to transfer it back out when funds run low.

Instead, focus on creating breathing room in your budget by understanding where your money is going and implementing changes when possible. A traditional budget, which you can also set up with Lunch Money, can help make this possible.