Zero-based budgeting, or ZBB, is a budgeting method that creates a job for each dollar you earn, ensuring none of your income goes to waste. It’s an effective way to prevent overspending, save money, and get out of debt.

So, how does a zero-based budget work? We explore how to set one up, the pros and cons of zero-based budgeting, and how to determine if it’s the right type of budget for you.

What is zero-based budgeting, and how does it work?

A zero-based budget is a spending plan for your money where every dollar you earn is earmarked for a specific purpose. In other words, you should have zero dollars left over after subtracting your expenses, including your savings, from your income.

If your monthly income is $4,500, the entire $4,500 should be directed toward spending, savings, debt, charitable contributions, etc. I’ll share a more detailed example later.

How to set up a zero-based budget

Before creating your zero-based budget, you’ll want to gather your bank account and/or credit card statements from the past few months. Figure out how much you’ve spent in different categories, such as groceries, gas, clothing, eating out, etc. Understanding your spending habits will help you create a realistic budget and identify areas where you may overspend.

Now that you have this information, it’s time to create your budget using the following steps:

1. Calculate your monthly income

Start by listing all of your monthly income sources. This could include paychecks from your employer, various government benefits, or income from a part-time job or side hustle.

Add up all of your earnings to get your total monthly income.

2. List your expenses

Your next step is to create your expense categories for the upcoming budget period, whether monthly or bi-weekly. You’ll also want to assign a dollar amount for each category. Consider everything you spend money on throughout the month. Here are some sample budget categories:

Fixed expenses (Needs):

- Mortgage/rent

- Food

- Gasoline

- Insurance premiums, e.g., auto, life, health, etc.

- Transportation

- Utilities

- Minimum payments on debt, e.g., loans, credit cards, etc.

Discretionary Expenses (Wants):

- Dining out (Restaurants, Coffee)

- Clothing

- Travel/Vacations

- Sporting events, concerts

- Subscriptions (Netflix, Spotify, etc.)

Other expenses:

- Additional debt repayments

- Savings/Investments, e.g., emergency fund, retirement savings

- Charitable contributions

- Irregular expenses, such as birthday or Christmas gifts

- Miscellaneous

This is not an exhaustive list, and the beauty of the ZBB is that you can tailor your budget categories to fit your needs. Because the zero-based budget requires you to allocate every dollar of income, you may want to create a miscellaneous category as a catch-all for unexpected expenses. This will allow you to quickly categorize any surprise bills that pop up.

3. Subtract your expenses from your income

Here’s where the fun begins! Subtract your total expenses from your total income. Remember, your goal is to get a zero result, with every dollar accounted for. Don’t worry if you don’t hit zero on the first try. It’s unlikely that you will, especially with your first few budgets.

If you still have leftover income you need to allocate, that’s good because it means your cash flow is positive. You can allocate the extra funds towards savings, investments, debt repayments, or fun.

If your expenses exceed your income, you’re spending more than you’re making, which isn’t healthy for your finances. To correct this, consider ways to reduce your expenses, particularly in discretionary categories, such as entertainment, restaurants, or travel.

Another option is to see if you can increase your income by picking up more hours at work, starting a side hustle, or selling stuff you don’t use anymore.

If you’re still struggling to get out of the red after making these adjustments, you might have to take more extreme measures, like downsizing your home or car, to lower some of your monthly expenses.

4. Monitor your transactions

Congratulations, you’ve created your first zero-based budget. But the fun doesn’t end here! You’ll need to monitor your spending and income throughout the budgeting period, ensuring that every transaction falls into the appropriate budget category.

That soy candle you bought off Amazon? Categorize it under shopping. Your grandmother gifted you $20? Add it to your income.

Does it sound like a lot of work? The truth is that zero-based budgeting is more hands-on than other budgeting methods, such as the 50-30-20 budget or the pay-yourself-first method. Thankfully, budgeting apps like Lunch Money are designed to support ZBB budgeting and can make the task easier. But more on that later.

5. Make your next budget

As your budgeting period expires, it’s time to start over and create your next budget. Although your budgets will likely look similar month-to-month, there are bound to be changes you’ll need to factor in for each period.

This is especially true for those whose income fluctuates, including commission-based employees, seasonal workers, or the self-employed. You might also have periodic expenses, like an oil change or other vehicle repairs, or a family birthday.

Regardless of your situation, try to anticipate any out-of-the-ordinary expenses you need to account for in your new budget.

Zero-based budgeting example

To illustrate what a zero-based budget might look like, here is a simplified monthly budget for Jane:

Monthly Income:

- Employment income: $4,900

- Side hustles: $1,200

Total income: $6,100

Monthly Expenses:

- Mortgage: $1,700

- Utilities: $300

- Car loan: $500

- Clothing: $200

- Groceries: $600

- Transportation: $300

- Insurance: $400

- Entertainment: $325

- Subscriptions: $75

- Savings - Emergency Fund: $500

- Savings - Retirement: $1,000

- Miscellaneous: $200

Total Expenses: $6,100

Income ($6,100) - Expenses ($6,100) = $0

As you can see, Jane’s zero-based budget is balanced, with every dollar being accounted for. However, she will want to monitor her monthly spending to ensure she doesn’t overspend in any category.

How does Lunch Money support a zero-based budget?

As mentioned, zero-based budgeting requires a more hands-on approach. Thankfully, Lunch Money has features that support zero-based budgeting, making it easier to fine-tune your budget and monitor your spending.

Using screenshots, here’s a glimpse at how a zero-based budget can work in Lunch Money:

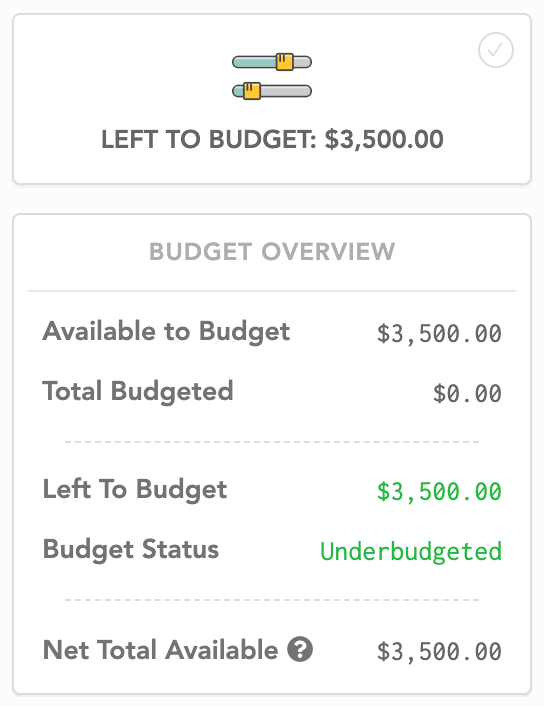

Before you assign your budgeted totals, Lunch Money lets you know how much income you have available for the month. Let’s walk through some Lunch Money screenshots to see how someone with a $3,500 monthly income might set their budget.

-

Lunch Money’s Budget Overview displays your total budget amount ($3,500, in this case). Your budget status will show as “underbudgeted” until you assign all of your income.

-

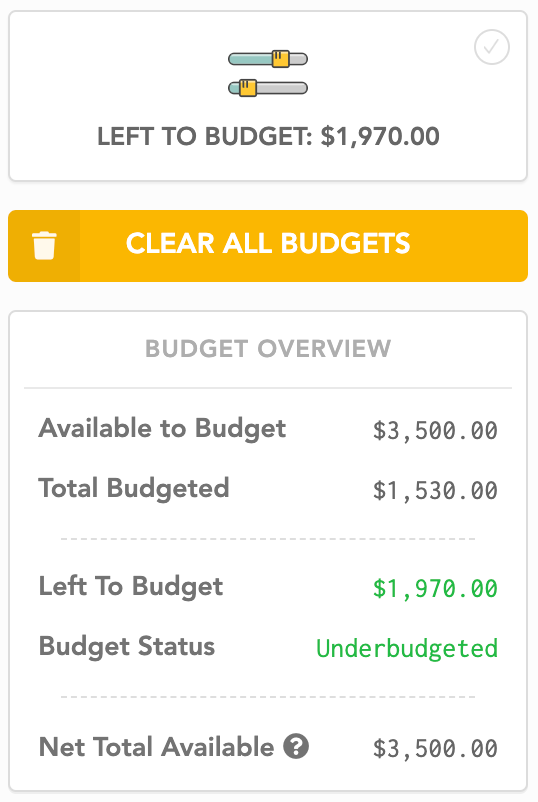

As you set your budget, Lunch Money will let you know how much you still need to assign to various budget categories.

-

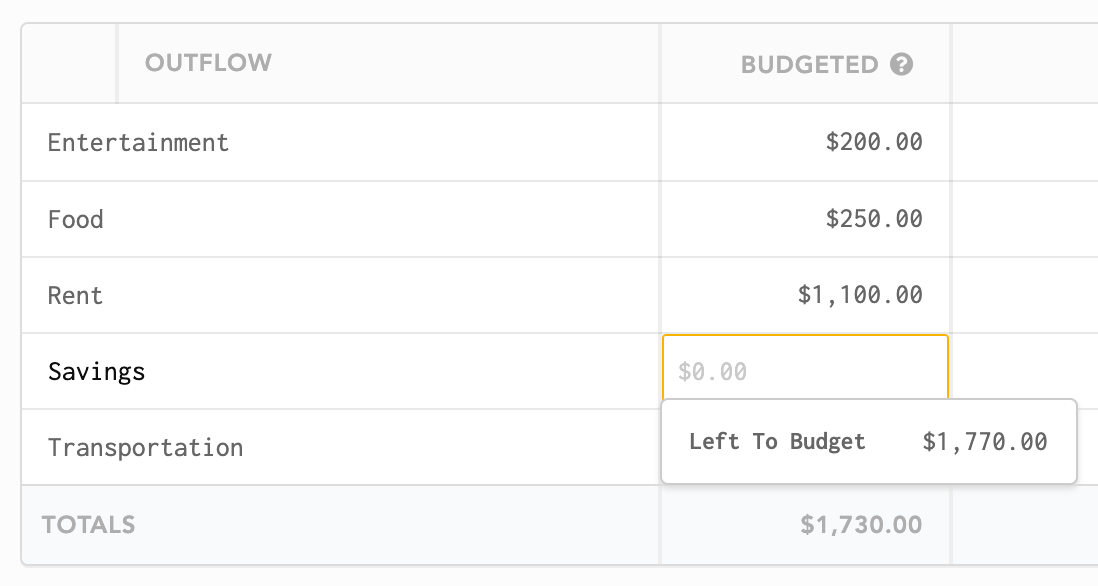

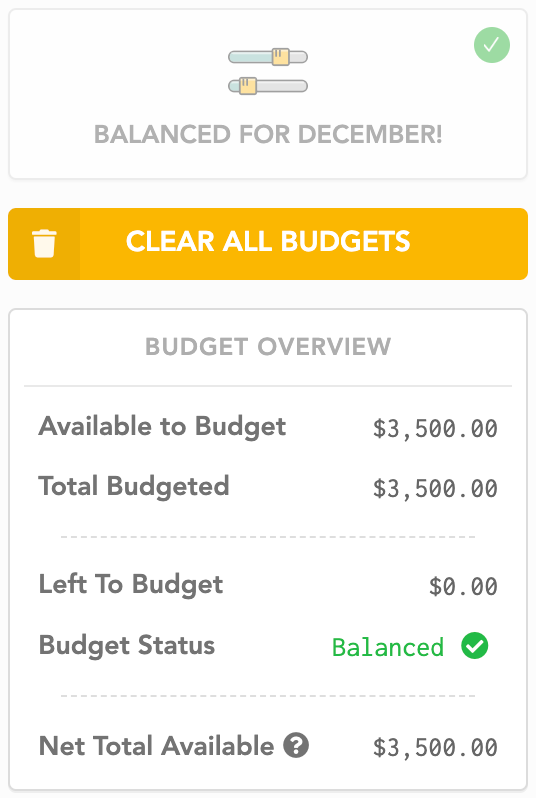

By the time you reach your last category, typically “Savings,” you’ll know exactly how much you need to assign to balance your budget:

-

Once every dollar from your income is assigned, Lunch Money will let you know that your monthly budget is balanced!

With Lunch Money, you can create as many budget categories as you want. For example, instead of having a single category to cover your monthly subscriptions, e.g., Netflix, Amazon Prime, Spotify, etc., you could create a separate category and assign a dollar amount for each subscription.

You can also customize your budget periods with Lunch Money. Want to reset your biweekly budget every second Friday? How about weekly, starting on Mondays? You can do that with Lunch Money.

Finally, Lunch Money supports account syncing and automatically imports your daily bank account and credit card transactions, sending them to the appropriate budget category. This makes monitoring your budget a breeze, helping you avoid overspending in any category.

Benefits of zero-based budgeting

See exactly where your money is going

With a zero-based approach to budgeting, there’s no longer any mystery as to where all your money went. You’ll always have a complete picture of exactly where it’s going.

If you’re ever in doubt, you can look at your past budgets and transactions so it doesn’t feel like your paycheck just disappeared.

Get the most out of your money

Since every dollar has a purpose, you can clearly define how much you spend and save, ensuring that none of your money goes to waste.

By creating a clear plan for your money, you can pay off debt, build an emergency fund, save for retirement, and meet any other financial goal you set your mind to.

Flexibility

What is the main characteristic of a zero-based budget? The fact that you can customize it however you want!

Whether you have an enormous mortgage payment, mountains of student loan debt, or fluctuating income, you can tailor your budget to accommodate your current financial needs.

Drawbacks of zero-based budgeting

Time-consuming

Since you must assign every dollar with a ZBB, you must review every transaction. It also requires you to continuously monitor your finances, not just when you set your budget, to ensure you stay on track.

Although time-consuming, this hands-on approach prevents overspending more than “set and forget it” budgeting methods.

It can be challenging if you have a fluctuating income

Zero-based budgeting can be more difficult without a fixed monthly income because you might not know how much income you’re working with at the start of each budgeting period. That’s not to say it won’t work for you; it’s just that the process is slightly different.

One option is to review your income for the past few months and use the lowest amount as your baseline. If you make more than that, you can allocate your additional income to a miscellaneous category and redistribute it at the end of your budgeting period.

Can be complicated

Even if your income doesn’t fluctuate, if your expenses change regularly, you might need to adjust your budget during the month for accuracy.

And if you overlook any substantial odd-ball expenses, such as an annual subscription fee, it may require you to rework it completely. Zero-based budgeting can also be challenging for those who struggle with impulse spending.

ZBB vs. the 50/30/20 budget

The 50/30/20 budgeting rule is a simple approach where 50% of your income goes to necessities, 30% to wants, and 20% to savings (or extra debt payments). It’s ideal for new budgeters or those who don’t want to get too involved with their budget.

However, not everyone’s spending fits into these strict boxes. For example, if you’re in a high-cost-of-living area, you’ll likely spend more than 50% of your income on needs. You get way more customization with zero-based budgeting.

ZBB vs. envelope budgeting

Envelope budgeting (often called “cash stuffing”) is similar to zero-based budgeting.

The primary difference is that you set aside physical cash for your expenses in physical envelopes—one envelope for each spending category. So, you’d have one envelope for rent, one for utilities, one for groceries, one for restaurants, and so on.

Once you run out of money in an envelope, you can’t spend any more on that category (unless you take cash from another envelope).

While this budgeting method can help you avoid impulse spending, carrying cash around can be inconvenient and less secure than keeping money in the bank.

Is zero-based budgeting right for you?

If you don’t mind getting into the weeds with your finances, zero-based budgeting could be the best method for you. While it takes a little more time and effort, ZBB gives you more control over your finances, so you know exactly where every dollar is going.

And you don’t have to do it alone! Lunch Money can help you plan your zero-based budget, track your spending, and reach your financial goals.