Do you ever feel like your budget doesn’t match the way you actually get paid? Unfortunately, most budgeting apps force you into a monthly cadence, which might not work well if you get paid weekly or monthly. The good news is that Lunch Money lets you set custom budgeting periods. This allows you to align your budget with your income and set flexible financial goals that actually make sense for your life.

Why Custom Budgeting Periods Matter

If you are paid weekly or bi-weekly, you likely plan your spending around each paycheck, setting aside money to cover your upcoming bills.

But most budgeting apps don’t work like that. They restart every month, forcing you to do a lot of mental math to figure out how much you can actually spend from each check.

Not only that, but not all months are created equal. For example, January has 31 days, while February only has 28. And if you grocery shop every Friday, what happens when a month has five Fridays instead of four?

The point of a budget is to make handling your money easier — not more complicated.

That’s where Lunch Money’s custom budgeting periods come in. They solve these problems by allowing your budget to match your paycheck. You decide ahead of time how much you need to set aside for bills and how much you can spend.

In other words, less mental math, fewer mistakes, and easier budgeting.

Custom budget period examples

While Lunch Money’s budget settings default to monthly, here are some examples of how you could customize your budget period:

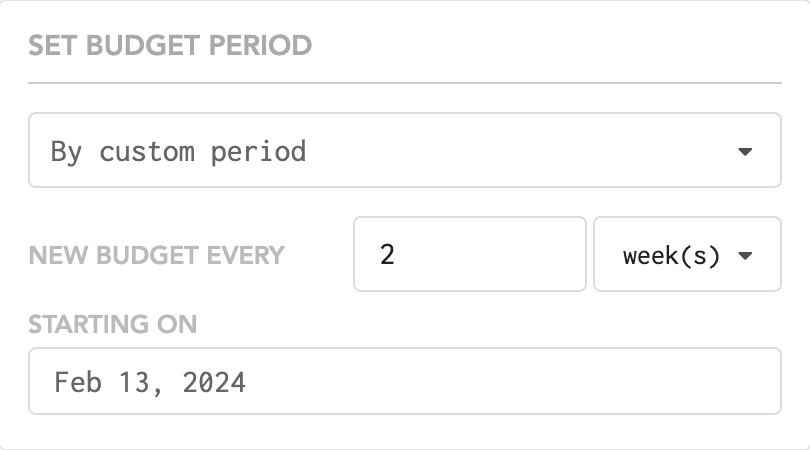

Scenario #1: Biweekly, starting on Thursdays

Solution: Set your custom budget period for “every 2 week(s), starting on Thursday, Feb 13, 2025.”

Scenario #2: Weekly, starting on Mondays

Solution: Set your custom budget period for “every week, starting on Monday, February 17, 2025.”

Scenario #3: Every 28 days

Solution: Set your custom budget period to “every 28 day(s), starting on March 1st, 2025.”

Scenario #4: Quarterly budget (4X per year), with the first quarter starting in April.

Solution: Set your custom budget period to “every 3 months, starting Tuesday, April 1, 2025.

Things to consider when choosing a budget period

Here are some decisions you’ll need to make when setting up your custom budgeting period.

How often do you want to set your budget?

You first need to decide how often to reset your budget. Shorter timeframes, such as one week, can help with tracking but require more frequent check-ins since you’ll need to address your budget every seven days.

Longer periods can be more manageable, but it can also be easier to get off track because you’re not required to check in as frequently.

Does your budget align with your paychecks?

Aligning your budget to your pay schedule makes sense. You’ll know exactly what you need to set aside between paychecks for larger bills, such as rent, and how much you can spend on items such as groceries and entertainment.

What about recurring expenses?

Not all your expenses will align with your budgeting period — for example, most people’s rent and car insurance are paid monthly. To account for this, when setting up a weekly or biweekly budget, set any leftover money in each budget category to roll over into the same category.

For example, let’s say your rent is $1,500 monthly, but you get paid every two weeks. When setting your bi-weekly budget, allocate $750 for rent, or 50% of the monthly amount. When the first of the month rolls around, you will have set aside the full $1,500.

Keep in mind that there are a couple of months each year where you will have three paychecks. In that case, you could adjust the rental amount to $500 for three periods rather than $750 for two. Or, you could zero out the rent category for the extra bi-weekly period that month.

This approach also works for annual expenses, like subscriptions, car registration, and insurance. You can start planning for these expenses now by putting a little bit aside each paycheck.

Can you automate your savings and payments?

Instead of rolling over unspent money into the next budgeting period, consider changing your savings or payment frequencies to align with your budget period.

For example, if you are paid biweekly and have a $1,500 monthly mortgage payment, find out if your bank can collect $750 biweekly instead.

You’ll also save some interest. Here’s how:

Let’s say you borrow $237,000 at 6.5% for 30 years. This gives you a mortgage payment of $1,498. If you pay monthly, you will pay a grand total of $302,280 in interest over the life of the loan. However, if you make a half payment every two weeks, you will pay $230,400 in interest over the life of the loan. That’s a savings of almost 25%!

This does include making a half payment even when you receive three checks in one month, so you’ll be making 13 monthly payments per year instead of 12. But this small switch will save you $70,000 in interest.

You can do the same for other loans or savings goals.

Which categories should roll over?

You don’t need to set all categories to roll over into the same category. Whether you’re following a zero-based budget, envelope budgeting, or the 50/30/20 budgeting method, you can keep leftover funds in a category or return them to the general pool to be reallocated to another category for the next budget.

Gas could be a good example of this. If you budget $50 for gas but only spend $40, you may not need that extra $10 sitting in the gas category.

However, with a category like restaurants, you might want to have the unspent money roll over into restaurants for the next period. You can be rewarded for being under budget during the last period by splurging on your next meal.

With Lunch Money, you can make these decisions on a category basis, allowing you to customize your budget fully.

Final thoughts

Custom budgeting periods are a game-changer. Traditional budgeting apps force you into a monthly cycle, which can be very challenging when money is tight.

By using Lunch Money to create a budget that aligns with your paychecks, you can get a handle on your money, not the other way around.