Most budgeting apps default to a monthly budget — which makes sense since most bills are monthly. But what if you get paid weekly? Or just prefer breaking things down into bite-sized chunks? Enter the weekly budget.

Sure, a weekly budget takes a little more effort since you’re setting a budget more often. But that’s not necessarily a bad thing. In fact, checking in weekly keeps you engaged with your money, makes it harder for sneaky expenses to slip through, and helps you stay on track.

Weekly vs. monthly budgeting — which one’s right for you?

The best budgeting period is the one that works for you.

A weekly budget is ideal if you’re paid weekly or want more frequent check-ins with your money.

A monthly budget works well if you already have a solid handle on your finances and don’t need to check in as often. Since most bills have a monthly cadence, this approach can be more flexible and easier to manage.

How to budget when you get paid weekly

A weekly budget isn’t much different from other frequencies, you just have to set it more often.

If you need some help getting started, here is a step-by-step guide:

Step 1: Determine your income

If you work a set schedule and your check is the same every week, this step is easy. On the other hand, if your income fluctuates, your best bet is to calculate your average weekly earnings. You can do this by reviewing your paystubs or bank deposits over the last few months. This will help you understand what your actual income is.

Pro tip: We tend to overestimate our income, especially when it varies from week to week. Be honest with yourself!

Step 2: List your fixed expenses and divide by four

Next, take all your monthly fixed expenses (rent, utilities, subscriptions, etc.) and divide them by four to determine your weekly fixed costs.

For example, if your rent is $1,600 per month, you’ll want to set aside $400 per week.

Heads up! Most months have more than four weeks, so if you get paid weekly, you’ll have four months each year where you get five paychecks. Decide now what you want to do with that extra money — boost savings, pay off debt, or treat yourself (responsibly).

Step 3: Get real about your spending

Once you know how much money is already spoken for (bills, savings, etc.), you can see what’s left for everything else. If you’re unsure how much you typically spend, scroll through your bank transactions from the last few months. This will give you a good idea of your current habits, but be prepared — it could be eye-opening.

Step 4: Set your weekly budget

You’re now ready to create your budget!

Start by setting aside money for your fixed expenses based on the amounts you determined in step two. Then, choose your spending categories and the amounts you plan to spend in each category. Don’t forget to set something aside each week for savings!

If you’re using Lunch Money, you can quickly choose from our list of default budget categories and create as many additional categories as you’d like.

You can also organize multiple categories into larger category groups. For example, under “Travel,” you could list “Flights,” “Car Rental,” “Accommodation,” “Food,” and “Tourist Activities.

Pro Tip: If you are new to budgeting, consider starting with fewer spending categories. You can always add more later!

Step 5: Adjust your budget as needed

A budget isn’t set in stone — it’s a living, breathing document. Some weeks will go smoothly, but it can also feel messy, especially when you are first getting started.

Consider each new week a clean slate and adjust as you become more familiar with your income and spending patterns. Don’t get discouraged when things don’t go as planned. The more you budget, the easier it will get.

Creating a weekly budget with Lunch Money

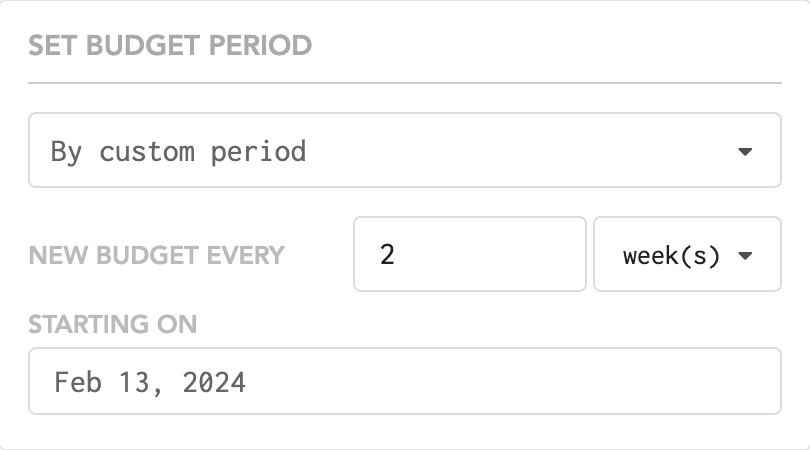

Lunch Money allows you to set custom budgeting periods, a feature no other major budgeting app supports. So, it can accommodate you if you want to budget weekly, bi-weekly, or monthly. You can also set your budgeting period to begin on any day of the week.

To find this feature, click on “Budget Settings” and then choose “By custom period.” You can then choose exactly how often you’d like your budget to reset.

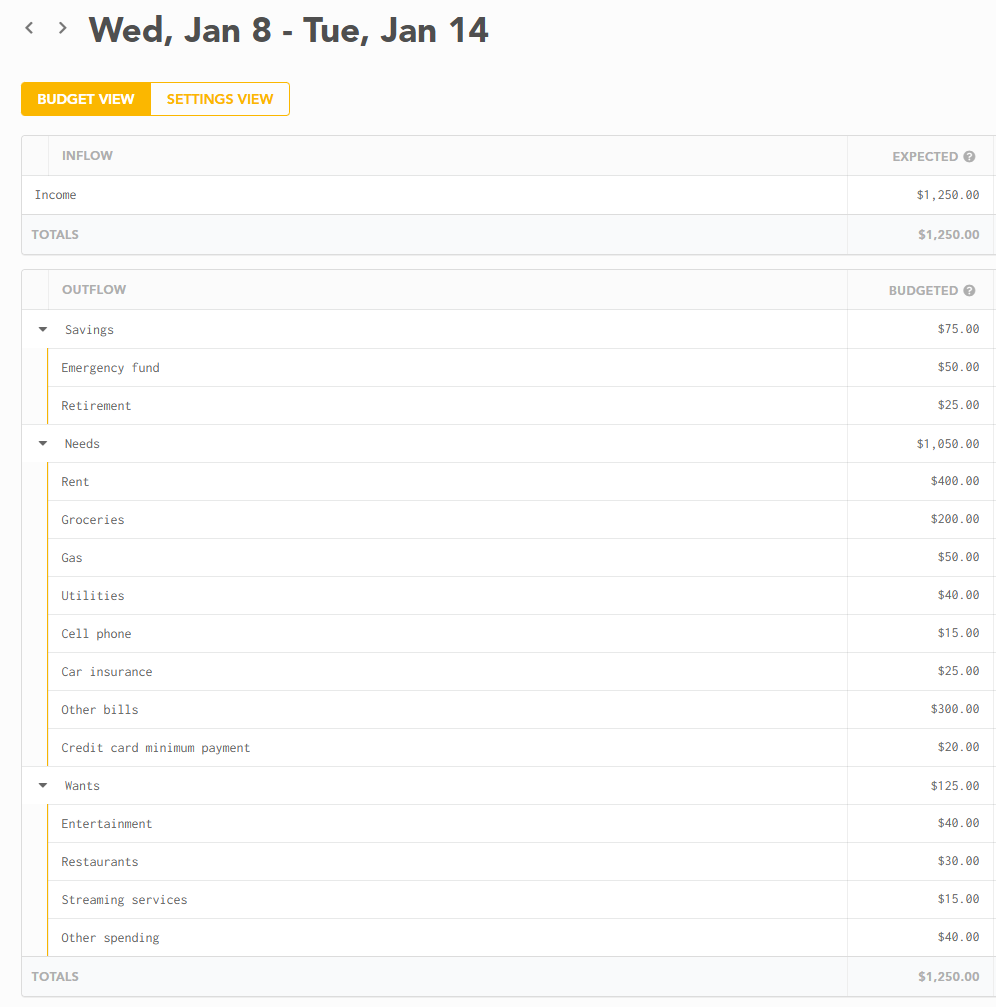

From there, set your income and planned spending based on your selected time frame. Here is what a weekly budget might look like:

You can choose what to do with unspent money in a category at the end of each week. Take rent, for example. You’ll likely want unspent money to roll over and stay in the same category. This way, you can build up your funds during the month and have it available when it’s time to pay your rent.

However, you might want any money left in the gas category to go back into the general pool of funds to be allocated for the next period. You may not need to build up extra funds in that category and choose to do something else with those leftover funds the following week.

Pros and cons of a weekly budget

Pros

- It aligns with your paychecks and is easy to conceptualize: If you get paid weekly, you likely think about your money on a week-to-week basis. Therefore, a weekly budget will fit right into your current habits. Short budgeting periods can be easier to manage: If you get off track, you only have to wait a few days before starting over. This can make budgeting feel easier as you get lots of fresh starts.

- A smaller budgeting window means less room for error: A weekly budget only includes about 25% of your monthly income, so a single spending decision can have a more significant impact. This forces you to be more mindful of every dollar you spend.

- Works with different budget methods: Most popular budgeting methods, including envelope budgeting, zero-based budgeting, and the 50/30/20 method, work with a weekly budget.

Cons

- Inflexible: Weekly budgets don’t offer much flexibility. One unexpected expense can throw your plan out of whack, making an emergency fund even more critical.

- Doesn’t align with most bills: Bills are typically paid monthly, so if you aren’t diligent about setting money aside in advance, you may not have enough when the bill is due.

- Time-consuming: A weekly budget requires you to set a new budget at least once a week. This takes more time than working with a monthly budget.

- Only works with weekly paychecks: If you get paid bi-weekly, a weekly budget probably won’t work for you. But no need to worry; Lunch Money also supports bi-weekly and monthly budgeting frequencies!

Managing unexpected expenses on a weekly budget

A weekly budget means you have less wiggle room for surprise expenses. If your car breaks down and you have to dip into your rent money to pay for it, next week’s budget just got a lot tighter.

By building an emergency fund, you can add a lot of flexibility to a weekly budget. Any money you can set aside will help. Even $5 or $10 per week will add up over time, eventually creating a solid cushion.

Final Thoughts

Whether you’re paid weekly or just want to be more hands-on with your money, a weekly budget can make a lot of sense. To budget monthly bills, set aside one-fourth of the funds each week. Also, consider your savings goals and set aside something each week for longer-term goals.

Finally, remember that an emergency fund is critical with a short budgeting period, as you have less flexibility. Having these extra funds set aside will allow you to absorb unexpected expenses more easily.