Living paycheck to paycheck is stressful and frustrating, especially when you’re doing your best.

Many households are in the same position. In a recent Leger study, 46% of Canadians and 57% of Americans reported living paycheck to paycheck.

Several factors can make it difficult to get ahead financially, including low income, debt, or no budget. The good news is that there are ways to break the paycheck-to-paycheck cycle and build more financial stability.

Reasons you’re living paycheck to paycheck

Before you can stop living paycheck to paycheck, it’s important to understand what’s causing it.

Income is too low

Living paycheck to paycheck isn’t always about overspending — sometimes it’s simply that you’re budgeting on a low income that hasn’t kept up with rising costs. Rent, groceries, insurance, and utilities have all gotten more expensive, making it harder for people to make ends meet.

When fixed bills take up most of your income, there’s very little room left to save or absorb surprise expenses. Even people with strong budgeting habits struggle when their earnings barely cover living expenses.

Too much debt

When a large share of your paycheck goes toward debt, it can be tough to get ahead. Credit cards, student loans, or car loans can quickly add up, taking up a large portion of your monthly income.

As your balances grow, minimum payments increase, leaving less room in your budget. And while paying only the minimum keeps your account in good standing, it takes longer to pay off your debt and increases the amount of interest you pay (keeping you stuck in the cycle longer).

No emergency savings

Without an emergency fund, surprise expenses, like a medical bill or car repair, can wipe out what’s left of your paycheck. When you don’t have a buffer, you may have to rely on credit cards or payment plans.

Setting aside backup savings helps you handle the unexpected without taking on new debt. Even a small buffer can keep your monthly budget on track.

Lifestyle inflation

Lifestyle inflation occurs when your spending rises alongside your income. For example, after a raise or promotion, you upgrade your car or dine out more.

Earning more money can give you breathing room, but only if your costs don’t increase with it. If every raise gets absorbed into a higher standard of living, there’s little left to save, invest, or use to break the paycheck-to-paycheck cycle.

No plan for your money

If you don’t have a clear plan for your money, it’s easy to overspend without realizing it, especially in areas like shopping or take-out. Setting limits for discretionary spending helps you stay in control of your money.

A basic monthly budget shows what you’re realistically able to save. After covering your essentials, you can allocate some toward your financial goals, then use the rest for fun.

How to break the paycheck-to-paycheck cycle

Now that you know what causes the paycheck-to-paycheck cycle, here is some advice to help you break it.

Know your numbers

The first step to breaking the paycheck-to-paycheck cycle is understanding exactly where your money’s going, including what’s coming in and what’s going out.

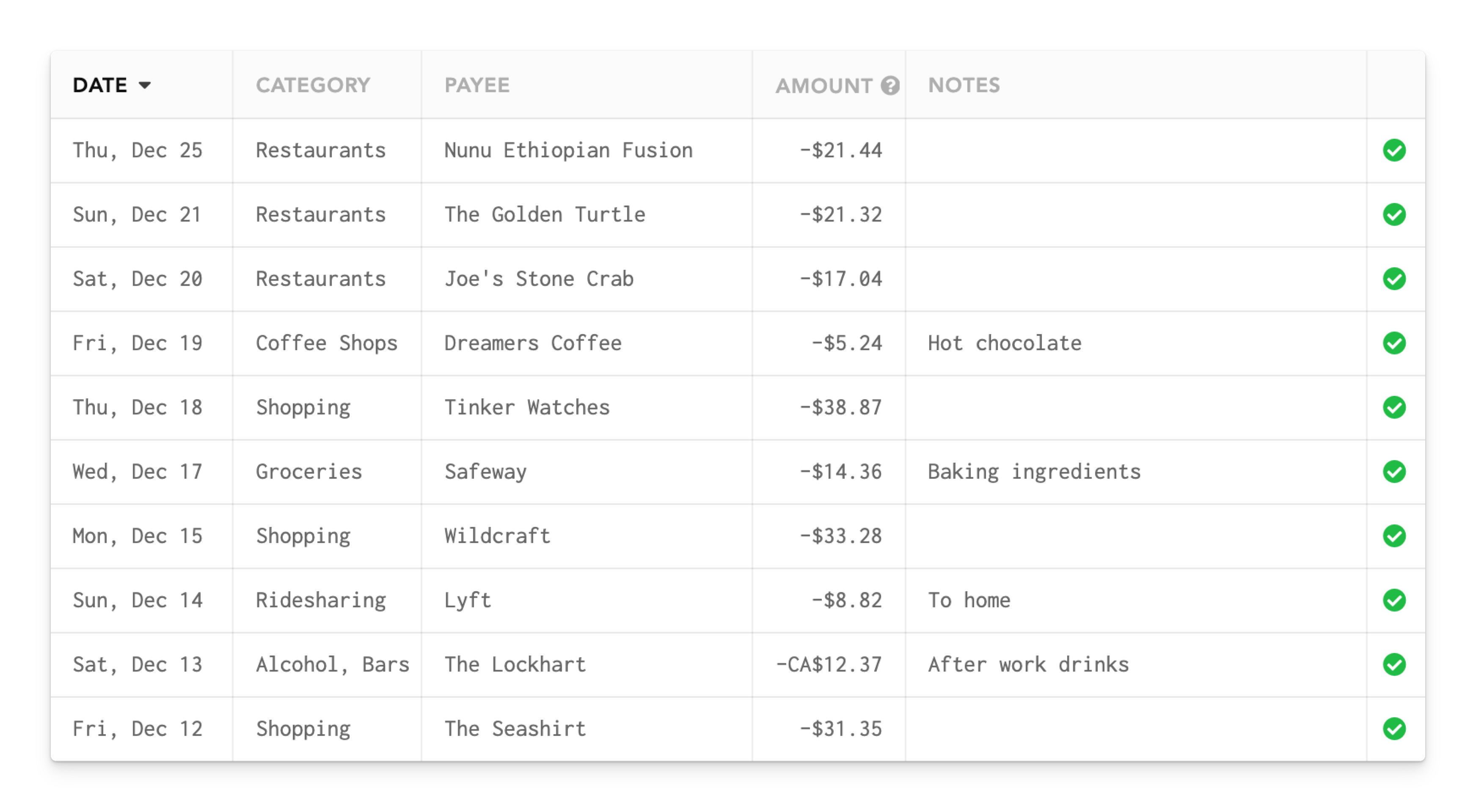

Start by listing your income along with fixed (costs that stay the same) and variable expenses (costs that change). If you sync your accounts with Lunch Money, it automatically categorizes your transactions and shows your recent spending patterns.

Build a survival budget

Next, create a budget that includes only the minimum expenses you need to live on. You should list all of your essentials, such as:

- Housing

- Utilities

- Transportation

- Groceries

- Insurance

- Child care

- Minimum debt payments

This stripped-down budget helps you see exactly how much you need to get by without any extras. Knowing your baseline makes it easier to plan your next move and start building savings.

Get one month ahead on expenses

Once you’ve built your survival budget, try to live on it while you build a one-month emergency fund. Your goal is to set aside enough to cover a full month of essential expenses.

This buffer removes the stress of paycheck timing because next month’s bills are already covered. As you keep contributing, you’ll see your savings grow from a few hundred dollars into thousands.

Use each paycheck with purpose

Instead of letting each paycheck disappear on who-knows-what, make a simple plan for it. Cover the essentials first, like housing, food, transportation, and minimum debt payments, so your core needs are covered.

Next, move some money to savings right away, even if it’s a small amount, to pay yourself first. Then, you can live off whatever’s left over, whether it’s for takeout, subscriptions, or going out with friends.

Make small cuts to your spending

If you want to save even more, look for minor cuts you can make in a few spending categories. Avoid making extreme budget cuts — just look for small ways to live frugally across multiple categories.

For example, if you normally spend $400 on food, try to reduce your grocery bill to $350. Gradual changes are usually easier to maintain and can add up faster than you’d expect.

Plan for irregular expenses

Some costs don’t show up every month, such as holiday gifts, car repairs, or annual fees. Since they’re not a part of your regular expenses, they’re easy to forget and can throw off your budget.

To prevent this, set aside a small amount each month in a separate account for periodic expenses. For example, you could save $40 each month for Christmas. By the end of the year, you’ll have saved $500 for gifts.

Increase your income

Sometimes the quickest way to break the paycheck-to-paycheck cycle is to bring in more income, even temporarily. Outside of raises or job changes, gig and side work can give you extra breathing room.

If you have a marketable skill, like graphic design or editing, you might consider freelancing. You could also try driving for Uber or selling unused stuff around your house to bring in extra income.

Put extra money away

If you get paid bi-weekly, you receive a third paycheck twice a year because some months have three paydays instead of two. That added check can help you grow your buffer even faster.

The same applies to any other extra money that comes your way, whether it’s a tax refund, cash gifts, or bonuses from work. Instead of spending it, consider setting most or all of it aside into savings.

Summary

When you’re living paycheck to paycheck, it’s difficult to put money away for the future. One small emergency can eat up whatever’s left of your income.

Luckily, you can break this cycle! Get started by knowing your numbers, creating a survival budget, and saving a month’s worth of expenses to finally get ahead financially. For more on this topic, check out this YouTube video from Jacob Wade, one of our Lunch Money team members!

You can also try Lunch Money for free with our 30-day trial and start building financial stability.