If you’ve ever hesitated to log into your bank account, felt overwhelmed by debt, or told yourself you’ll start budgeting next month, you’re definitely not alone.

The good news? You don’t need an MBA or superhuman willpower to get your finances under control. With the proper process, you can go from anxious to confident and in charge of your money. In this guide, I’ll walk you through my simple 4-step framework to help you get clear on your finances, build a plan you can actually stick to, establish habits that support your goals, and pay off debt and build long-term wealth.

With tools like Lunch Money, you can track everything in one place and see your progress in real time.

Step 1: Awareness - Get clear on where you currently stand

Awareness is a BIG first step, because facing your numbers can feel intimidating. But you can’t change what you don’t understand, so this step matters. Here’s what I recommend:

-

Make a list of your assets and liabilities: everything you own (assets) and everything you owe (debts or liabilities). Assets can include checking and savings accounts, investment and retirement accounts, vehicles, and real estate.

When listing your debts, make sure you include the following information:

- Who you owe

- The total balance

- Interest rate

- Minimum monthly payment

- Due date

-

Review your spending (Optional but extremely helpful): Looking at the past 3-6 months of transactions will be eye-opening, but you’ll start to notice where you tend to overspend, categories that surprise you, expenses that you can reduce or eliminate, and what actually matters to you (vs. impulse spending).

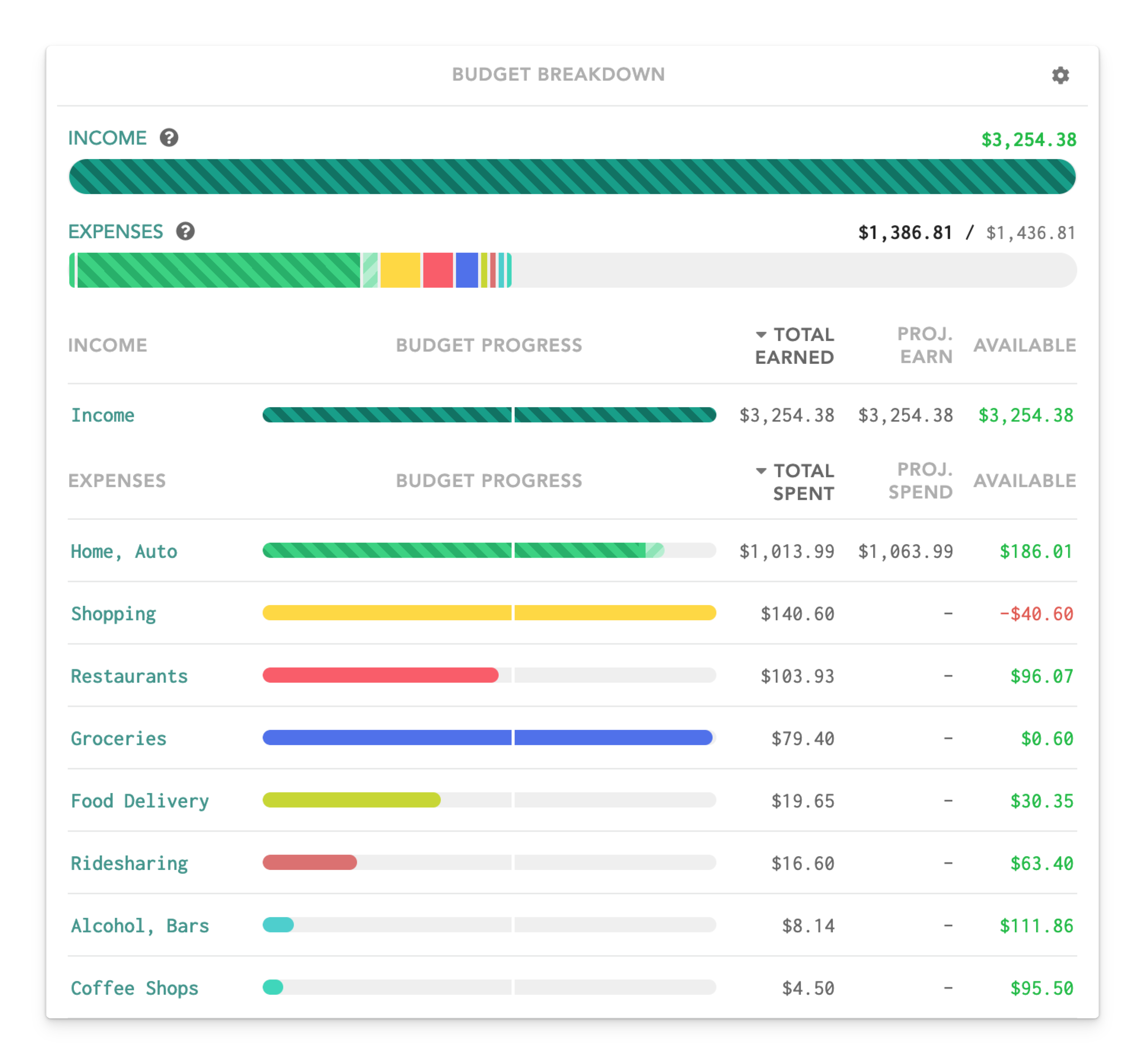

This is a great time to link all of your accounts with Lunch Money. Once everything syncs, you get a full picture of your finances in one dashboard, and your numbers update in real time!

- Set some financial goals: Now that you have a complete picture of your finances, give some thought to what goals you would like to work toward. This could be building an emergency fund, paying off all credit card debt, starting to invest $100 each month, etc.

These goals will inform the next steps.

Step 2: Budget & optimize - Create a plan that fits your life

I know, I know, it’s the dreaded ‘B’ word. Budgeting has a reputation for being restrictive, but a smart budget isn’t about depriving yourself; it’s simply a plan for your money.

Before creating your first budget, you’ll need to figure out your expected income and your monthly expenses, including all minimum debt payments. From there, you can:

How to create a budget that fits your actual life

Using Lunch Money, enter your income for the month. Then build your budget using the categories that are relevant to you. Here’s a list of common budget categories to get you started:

- Rent/mortgage

- Utilities

- Groceries

- Food out

- Car fuel

- Car insurance/any other insurance

- Subscriptions

- Childcare

- Pets

- Fun/entertainment

- Personal

- Health/Wellness

- Self-care

- Gifts

- Travel

- Debt payments

- Savings/Investments

Keep in mind that every month will look a little different. That’s completely normal and exactly why you’ll want to create a new budget every month.

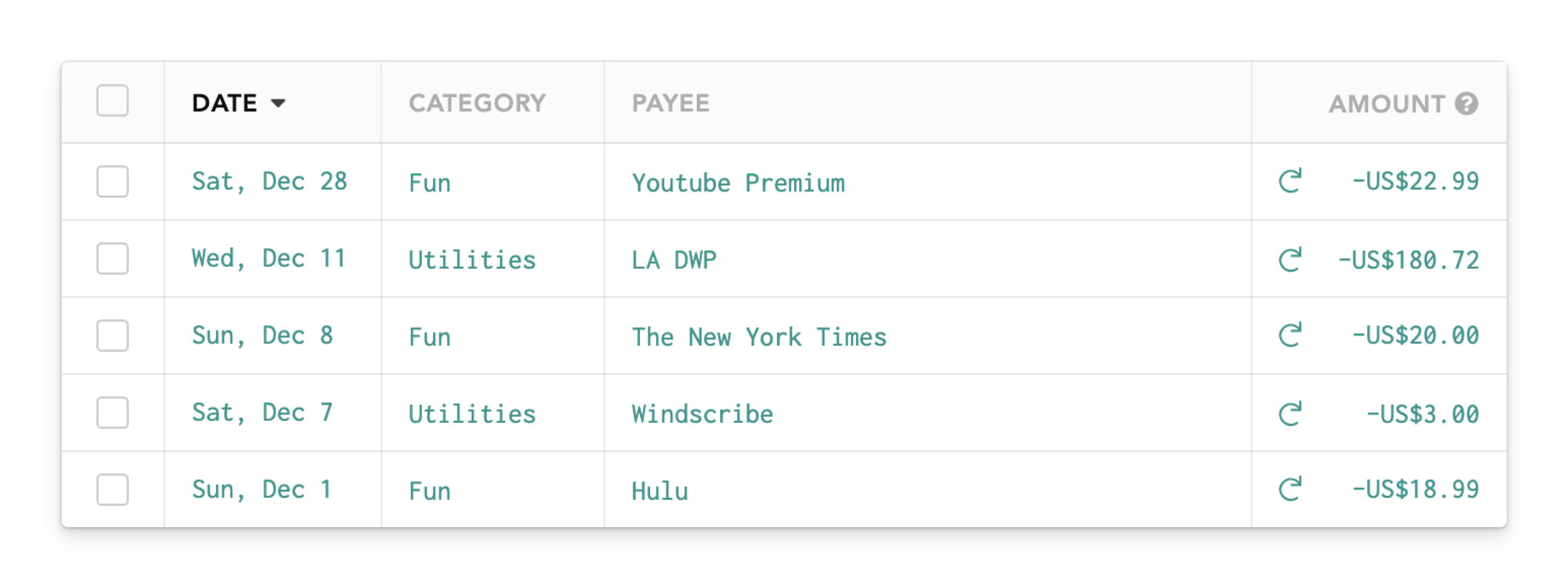

Lunch Money Tip: Gather similar expense categories under a larger category group for better organization. For example, you can use a ‘Fun’ category for recurring expenses such as Netflix, Hulu, Spotify, etc. Then you’ll be able to quickly and easily see how much you’re spending in that area!

Start weaving your financial goals into your plan

For example, if one of your goals is to build your emergency fund to $3,000, you can allocate ‘leftover’ money from your budget toward that goal before you make extra debt payments.

Step 3: Systems & Habits - Build consistency (this is where change happens)

You can create the most beautiful budget in the world, but without consistent habits, nothing sticks. This step is about building simple, sustainable systems that help you get results (and have fun along the way)!

Establish a weekly money check-in

Lunch Money automatically pulls in your transactions, but it’s up to you to review them. Choose one day each week, put it in your calendar, and make it part of your routine. Make it fun. Get cozy, grab some coffee or tea, turn on music, whatever works for you!

During your check-in, review the following:

- This week’s spending

- Your budget vs. your actual spending

- Progress toward your goals

- Any adjustments needed for next month

Pro tip: Automate where you can. Automation reduces decision fatigue and helps you stay consistent even during chaotic weeks. Try to automate things like:

- Minimum debt payments

- Savings or sinking fund transfers

- Retirement contributions

- Recurring bills

Again, this means fewer decisions and keeps you on track even on the weeks where life feels chaotic.

Build habits that support your goals

Building habits takes time, but slow, steady, consistent action will help you get to where you want to be. Here are some examples of regular activities you might want to implement:

- Those weekly money check-ins

- Meal planning to reduce food costs

- Checking your budget before you make purchases

- Paying your credit cards off every payday

- Sending any extra income toward your debt or other financial goals

Step 4: Build - Pay Off Debt and Grow Real Wealth

Now that you have clarity, a budget, and consistent habits, here are four critical areas to focus on to make meaningful progress!

Build an emergency fund

An emergency fund is a buffer that prevents you from relying on credit cards when unexpected expenses arise, whether it’s a leaky faucet or a sudden car repair. While most experts recommend saving 1-3 months of expenses, you can start with $500 or $1,000 if money is tight. The important thing is to get started.

Focus on debt payoff (strategically!)

Debt works against your wealth. Interest grows, and the monthly payments drain your cash flow.

A common mistake I see people make is spreading extra payments evenly across their debts. This actually slows your progress!

Instead, choose one of the following debt payoff strategies:

- Debt Snowball: pay off the smallest balance first

- Debt Avalanche: pay off the highest interest rate first

- Cash-flow method: pay the debt with the largest minimum payment first

- Urgency method: pay the debt that causes the most stress first

Make minimum payments on all other debts, and put all your extra money toward your focus debt. Once it’s gone, roll that payment into the next one, and repeat!

Choosing a method and sticking to it is very important. And keep in mind that consistency matters more than making the ‘perfect’ choice; you can always switch later.

Start investing (when you’re ready)

If you still need an emergency fund or have high-interest debt, focus there first. But if your employer offers a retirement plan match like a 401(k) (or RRSP in Canada), consider contributing enough to secure the full match, because it’s essentially free money. Even $25-$50 per month can make a huge difference over time.

And keep in mind that investing isn’t about timing the market or trying to pick the right stock, it’s about:

- Making consistent contributions

- Choosing low-cost, diversified investments

- Focusing on time in the market, not timing the market

Think broad index funds and ETFs.

Track your net worth and milestones

In addition to helping you budget, Lunch Money also tracks your net worth automatically each month and breaks down increases and decreases across your debts and liabilities. Some months, your net worth will increase; some months, it won’t.

Progress isn’t a straight line, so don’t let this number define anything about you or your journey. That said, with time and consistency, you will experience:

- Your debt going down

- Your savings going up

- Your spending habits improving

- Your investments growing

- Wins you didn’t expect

- Months where everything clicks

- And more

Celebrate those wins!!

Paid off a credit card? Reached $1K in savings? Tracked your spending consistently? Celebrate it. You could treat yourself to something, but this doesn’t necessarily mean spending money. You could celebrate by baking some cookies, binge-watching your favorite show, giving yourself a slow morning, or doing anything that feels rewarding and keeps you on track.

Final thoughts: Progress, not perfection

I packed a lot of information into this article, but there is no need to do everything at once. Remember to start small by linking your accounts in Lunch Money, getting clear on your numbers, creating a realistic plan, and showing up consistently.

Small steps repeated consistently lead to huge results, and it DOES get easier with time. And if you’re based in the U.S. and feel like you could use personalized support, accountability, and a clear plan tailored to your situation, I’d love to help you through 1:1 coaching!