If you were born between 1965 and 1980, chances are you and I have a lot in common. Nostalgic memories of childhood often mix with today’s realities, which include high inflation and rising living costs, retirement worries, and the pressure of being part of the “sandwich generation”. Many GenXers are caring for aging parents while still supporting young adult children, all while trying to stay afloat.

This guide explores why budgeting is different for GenX and shows you how to build a money system that works for your life today.

Why budgeting matters more than ever for GenX

Our parents also dealt with financial uncertainty, but money worked differently back then. Cash was king, frugal living was considered normal, and budgeting was as easy as getting out a pencil and paper.

Today is different. Spending is easier and less visible with credit cards and contactless payment options like Apple Pay. Credit card balances are at record highs, and many households are feeling squeezed.

Housing costs are also much higher than what our parents paid for their first home. According to CNBC, the median home value in the U.S. was $38,100 in 1975. Adjusted for inflation, in 2024, that same amount would be $228,404. Today, a typical homebuyer must spend 5.3 times their income on a home, making single-income households nearly impossible in many areas.

Then there’s the emotional and financial reality of being part of the “sandwich generation”, caring for aging parents and young adult children at the same time. With income stretched in these different directions, many are finding it difficult to set aside money toward retirement.

But here’s the encouraging part: A thoughtful budget can provide clarity and a sense of order, helping you feel more in control over your finances.

Money strategies for the Sandwich Generation

As stated above, many GenXers are helping provide financial assistance to aging parents and their children simultaneously. Money can only go so far, so it is important to make a plan. Here are some strategies you can start employing today:

1. Analyze your income and expenses

List your income and expenses clearly, and you can see how much is still available to help your parents or adult children. If your take-home pay doesn’t provide extra funds to help, consider adjustments: Are there expenses you can reduce? Is there a way to increase your income?

2. Account for family support in your budget

Consider adding a separate “Family Support” expense category to your budget. If using category groups, you can create sub-categories for specific expenses, such as Senior Living costs or Parent Plus Loan costs.

This is also a good opportunity to find additional room in your budget to catch up on retirement savings. Intentionally setting aside money, even if it seems like a small amount, will help you feel better about your longer-term financial goals.

3. Communicate

Once you’ve set your budget, talk with your family and be honest about what you can afford to provide in terms of financial assistance. Having a conversation with other family members can be an opportunity to share the load and set a good example for the next generation.

How to choose a budget method

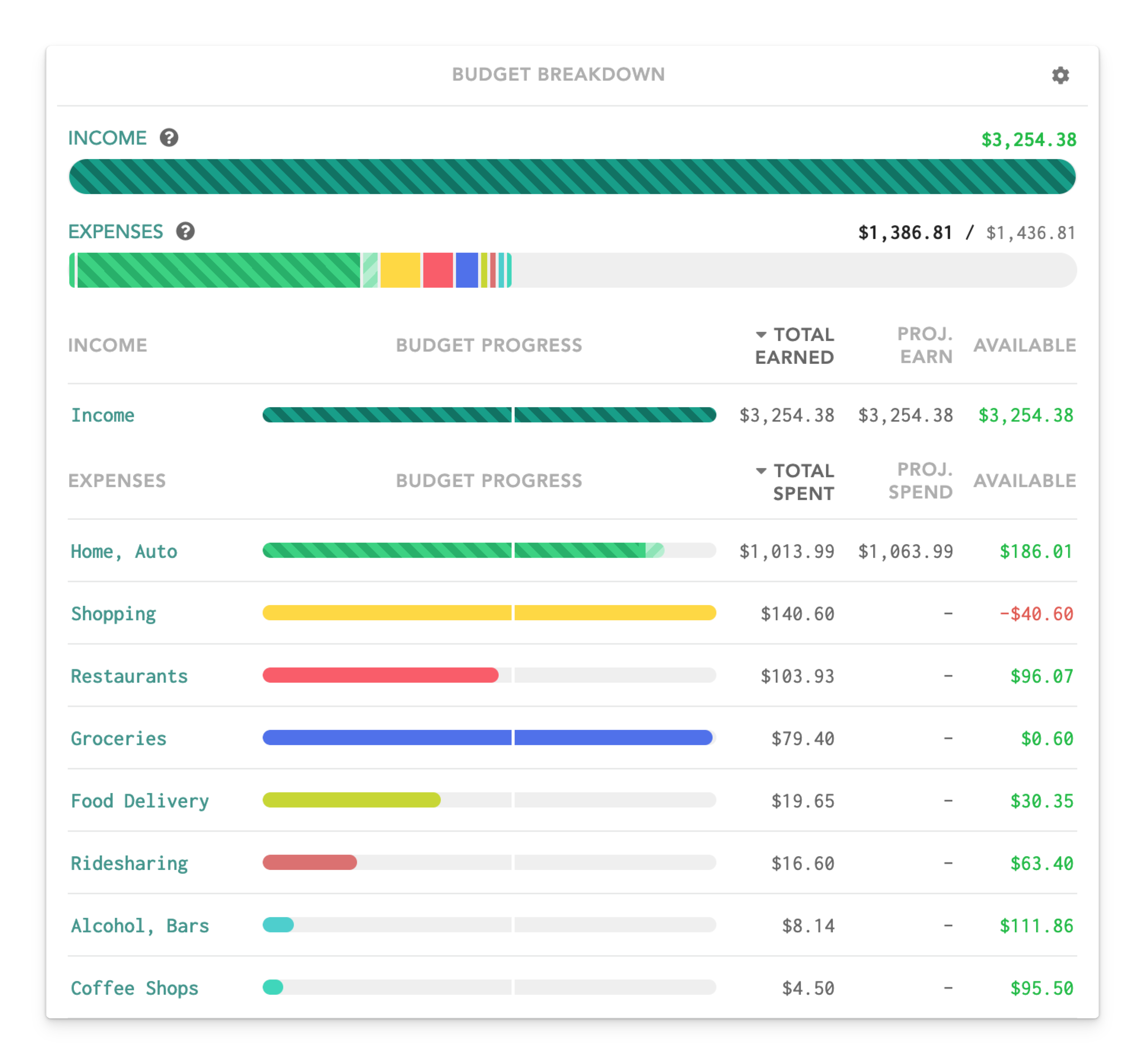

There is no right way to budget. As long as the system you choose helps you achieve financial clarity, it is a good setup. Whichever budgeting style you select, Lunch Money can help by providing insight and financial clarity.

With that in mind, here are some popular budgeting methods:

Zero-Based Budgeting

Zero-based budgeting, or ZBB, forces you to make a plan for all of your income. Each time more money arrives, you will assign those new dollars to jobs. All income is accounted for in this method.

The result should be: Income - Expenses (including things you’re saving for) = Zero.

This type of budgeting is very helpful for people wanting to get out of debt. Lunch Money lets you give every dollar a job and roll over dollars in categories of your choice. It also shows you how much you have left in a budget category and lets you cover overspending from another category.

Plan vs. Actual Method

With this method, you can plan out the entire period or month of spending before the money comes in. As spending is tracked throughout the month, it is compared to your original budget plan.

This type of budget is good for users who know precisely how much pay they take home each month and prefer to forecast what will happen. Lunch Money also supports a plan vs. actual approach. You can still see overspending or how much money is available in a category, and each period, you can quickly rollover your budget to the exact numbers from last month.

50/30/20 Budget

The 50/30/20 budget simplifies things by suggesting you spend 50% of your pay on needs, 30% on wants, and 20% on savings and debt repayment. Lunch Money allows you to easily set up budget categories in a Needs/Wants/Savings & Debt format. While this is a popular budgeting method for all income levels, it may not be a good option for high-cost-of-living areas or for those who want to prioritize paying off debt.

Final thoughts on Budgeting for GenX

GenXers may be dealing with new financial stresses, but we can be resilient. By analyzing our current financial situation, budgeting for our spending and goals, and communicating with others, we can begin to have clarity about our plan.

Like the Choose Your Own Adventure books we read as kids (remember those?), we can choose where to take our finances, and it is okay to make changes along the way. Don’t be afraid to ask for help. Financial coaches, like myself and others, are becoming more popular these days and are happy to help people who feel like they just need some hand-holding or encouragement.