We’ve all been there. You go to the store for milk, but somehow walk out with snacks, new clothes, and maybe a scented candle.

Impulse buys feel good in the moment, giving your brain a quick dopamine hit. But over time, they can pull you off track from your financial goals, like paying off debt or buying a home.

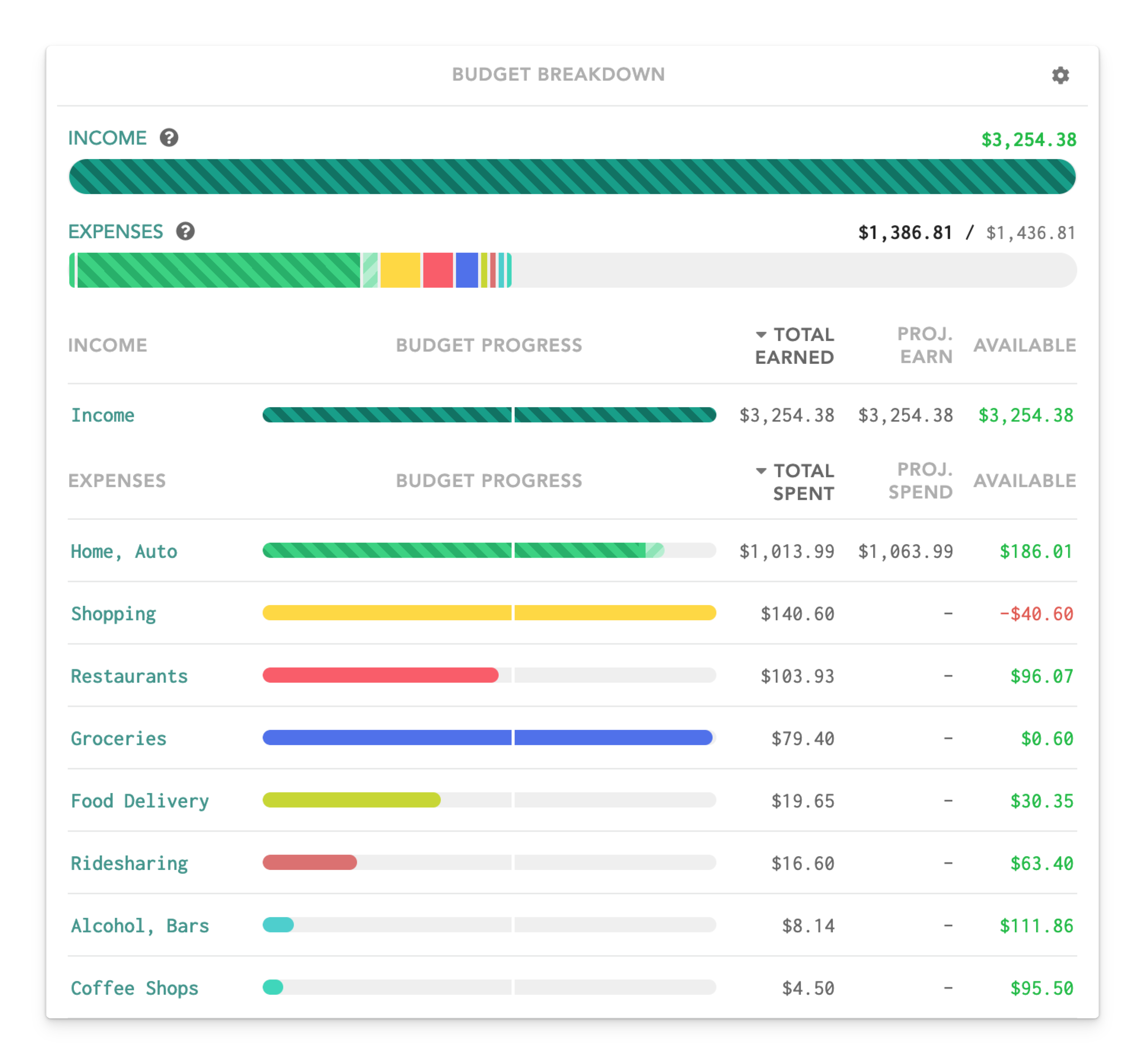

The good news is you can actually budget for impulse purchases with an app like Lunch Money. And once you pair it with the tips below to reduce impulse spending, you’ll feel even more in control of your money.

10 ways to reduce impulse spending

1. Use a 24-hour (or 30-day) waiting rule

When you see something you want, whether at a store or online, it can feel like you need to buy it right now. But giving yourself time before purchasing lets the initial dopamine spike wear off, making it easier to judge whether you truly need it.

I recommend setting a waiting rule based on price. For example, for smaller purchases, you could wait at least 24 hours before pulling the trigger. For bigger buys, like furniture or tech, stretch it to a week or even 30 days.

When you check back after the waiting period, ask yourself: Do I still want this? Does it fit a need? Does it align with my budget?

2. Keep a “wish list” instead of buying immediately

When you find something you want, you can also try adding it to a wishlist instead of buying it right away. This lets you enforce your 24-hour or 30-day rule while still keeping track of the item if you decide to buy it later.

Once you’ve paid yourself first and covered all your bills, you can return to your wishlist and prioritize which items you want the most. Remember, it’s okay to treat yourself as long as you budget for it.

You can even share your wishlist, so family and friends know what gifts to get you around your birthday or the holidays.

3. Remove saved credit cards from online stores

Retailers like Amazon know that the easier they make it to buy something, the more likely you are to do it. Features like “Buy Now with 1-Click” remove all the friction, so you can spend before you even have the chance to think about it.

Removing your credit card information from online stores can add a layer of inconvenience. If you have to get up, grab your wallet, and manually type in your card number, you may be less likely to spend.

4. Unsubscribe from promotional emails

When you shop online, you’ll often see pop-ups saying, “Sign up for our newsletter and get 15% off!” Brands use these offers to get you on their email list so they can send ongoing promotions and tempt you to buy more in the future.

Signing up can help you save a little at checkout if you’re already planning to make a purchase. However, after you receive the welcome email, scroll to the bottom and unsubscribe. This stops future promotional messages, helping you reduce impulse spending later.

And while we’re on the topic of “unsubscribing”, this might be a good time to cancel paid subscriptions that may have started as an impulse purchase but are no longer adding value to your life. Check out our list of 7 subscriptions you should consider cancelling, along with a few you might want to keep.

5. Avoid browsing stores and apps for “fun”

Sometimes it’s fun to window-shop, but it can lead to unplanned purchases. Even if you’re “just looking,” you’re putting yourself directly in the path of temptation, making it harder to live within your means.

If you tend to browse stores out of boredom, try swapping the habit for something that doesn’t trigger spending. For example, you could download the Libby app, which connects to your local library and lets you borrow e-books and audiobooks for free.

6. Shop with a list only

Grocery stores design their layouts to make you spend more. They place baked goods at the entrance, candy near the register, and milk and eggs (staples most people need) in the back, so you have to walk past dozens of tempting products.

To avoid falling into these traps, make a strict rule to stick to your grocery list. If you want to treat yourself, allow one fun purchase under a set dollar amount. This lets you enjoy spending spontaneously without blowing your budget.

7. Block or filter shopping ads

You can’t go online without getting hit with ads, and many of them follow you across multiple websites. Retailers track your browsing behavior so they can show you the exact items you’re most likely to buy.

If you clicked on a cool jacket once, you’ll suddenly see it everywhere, even if you’re trying to reduce impulse spending or stay on a “no spend” challenge.

One way to reduce this temptation is by using an ad blocker. Many browsers offer extensions that hide or filter ads before they load. You can also change your privacy settings or turn off personalized ads on platforms like Google, Facebook, and Instagram.

8. Use cash or debit only for discretionary categories

When you’re swiping a credit card, it’s easy to overspend, because there’s no immediate sense of loss since the bill doesn’t come till later. Switching to cash or debit for discretionary budget categories creates a clear spending limit.

You can preload a debit card or put a set amount of “fun money” into a separate account each month. Some people also find success using the envelope budgeting method. Once that money is gone, you stop spending in that category until your budgeting period resets.

9. Identify emotional triggers

As I mentioned earlier, a lot of impulse spending isn’t about the item, but the feeling you get when you buy it. Many people spend when they’re bored, stressed, or overwhelmed, using “shopping therapy” to boost their mood.

While that dopamine rush feels good in the moment, it usually fades as quickly as it comes.

Start by noticing when you tend to shop impulsively. Is it late at night? On stressful work days? When you’re lonely or procrastinating? Once you understand your triggers, you can recognize and avoid them.

10. Create alternative habits

Now that you know what sparks your impulse shopping, you can build healthier habits to replace it.

Physical activity works well because it boosts dopamine and serotonin. Studies show that exercise can help reduce stress and improve your mood, making you less likely to rely on shopping or other quick fixes.

If you don’t feel like breaking a sweat, you could also try simple swaps like making tea, journaling, or calling a friend.

How to Curb Impulse Spending with Lunch Money

It can be challenging to reduce impulse spending, but you don’t have to do it alone! At Lunch Money, we’ve created a budgeting tool that helps you stay on track with your financial goals.

When you sign up with Lunch Money and sync your accounts, it will automatically sort your transactions into different budget categories. That way, you can see exactly how much of your paycheck is going toward discretionary spending, like shopping.

Once you know where your money’s going, you can create a realistic budget that lets you pay all your bills, set money aside for savings and debt, and still include some fun purchases. Then you can regularly monitor your spending to make sure you stay within your budget.

Summary

Impulse purchases can be fun in the moment, but it’s important to keep them in check so they don’t derail your progress toward better financial health.

Simple strategies, like identifying triggers and creating alternative habits, can help you reduce impulse spending, freeing up more money for savings and debt payoff.

Plus, with Lunch Money, you can even plan for impulse buys by building them into your budget. That way, you can still have fun without impacting your financial goals. Try it out today with our free 30-day trial!