If tracking every dollar makes your eye twitch, the 75/15/10 budget might be your new best friend. It’s simple, savings-focused, and best of all, low stress.

Here’s how it works, how it stacks up against the ever-popular 50/30/20 rule, and how to make it work with tools like Lunch Money.

75/15/10 vs. 50/30/20 Budget: What’s the difference?

The 50/30/20 budget splits your money into needs, wants, and savings. The 75/15/10 budget says, “Nah, let’s keep it simple.” It puts all your spending into one category (the 75%). Then it divides the savings into long-term (15%) and short-term (10%).

To summarize:

- 50/30/20 = spending-focused

- 75/15/10 = savings-focuses

The 75/15/10 budget is perfect for people who don’t want to stress over how they spend their money. As long as you are meeting your savings goals, you’re good.

Here is an example:

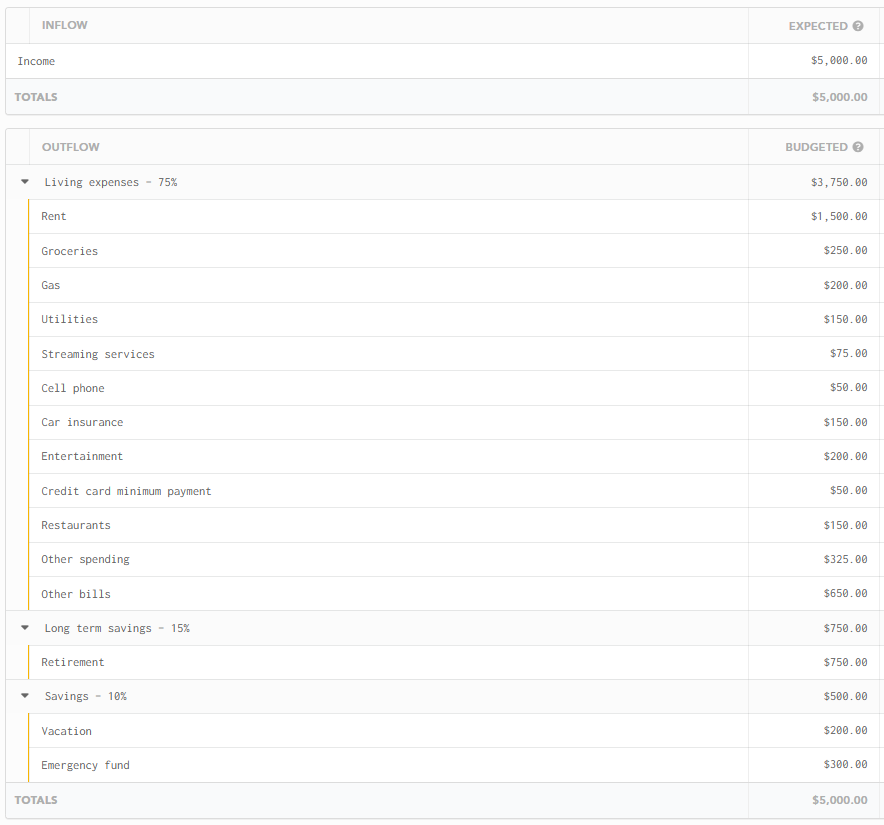

As shown in the image, this person has an expected income of $5,000. In a 75/15/10 budget, $3,750 can be used for needs, $750 for wants, and $500 for savings.

Living expenses break down like this:

- Rent: $1,500

- Groceries: $250

- Gas: $200

- Utilities: $150

- Cell Phone: $50

- Car Insurance: $150

- Credit Card Minimum Payment: $50

- Other bills: $650

Long-term savings break down like this:

- Retirement: $750

Finally, short-term savings are split into an emergency fund and a vacation savings account:

- Emergency Fund: $300

- Vacation: $200

Of course, your budget breakdown will differ. The beauty of the 75/15/10 method is that it’s super simple. As long as you are meeting your long-term and short-term savings goals, you are free to spend the rest of your money as you wish.

How to use the 75/15/10 budgeting method in Lunch Money

Setting up a 75/15/10 budget in Lunch Money is super easy. All you need to do is set your income and three category groups. This allows you to group your individual expenses so you can see how much you are spending as a group.

With the 75/15/10 budget, consider setting up the following category groups: “Living expenses,” “Long-term savings,” and “Short-term savings.”

In this Lunch Money YouTube video, our very own Jacob Wade walks you through setting up a 75/15/10 budget in the app. The tutorial starts around the 11-minute mark.

75/15/10 Budgeting Tips

Thinking a 75/15/10 budget might be the right one for you? Here are some best practices you can follow:

Automate your savings: Since the 75/15/10 budget focuses on savings, it helps to set up automatic contributions to your savings. If you have a retirement plan through your work, contributions are likely already automated. Still, you can also automate your contributions to your other tax-advantaged or non-registered savings plans.

Use separate accounts: If you are saving for multiple goals, use separate savings accounts for each goal. Doing this lets you keep track of exactly how much you have saved toward each goal.

Build in fun money: This is a great budgeting tip in general, not just for the 75/15/10 budget. It’s easier to stick to a budget long-term if you can have some fun once in a while.

Monitor your spending: How much you spend directly impacts how much you can save. Make sure to keep an eye on your spending so you can ensure you always meet your goals.

Remember, budgeting apps like Lunch Money make this super easy.

Give yourself grace: Changing your habits isn’t easy and won’t happen overnight. If you are currently spending 100% of your income, you can’t expect to reduce it to 75% in one month. Move towards that goal slowly and give yourself time to adjust. You don’t have to get it perfect tomorrow.

75/15/10 Rule alternatives

There are several different budgeting methods to choose from, each with its own benefits and drawbacks. If one doesn’t work for you, try another.

Envelope budget method (cash stuffing): With this budget, you take your spending money in cash and divvy it up into physical envelopes. This method works great for keeping spending in check, since you see physical cash leave your hand. However, it doesn’t work well if you do most of your spending digitally, or if you are nervous about carrying around large amounts of cash.

Learn more about the envelope method here.

Zero-Based budgeting (ZBB): With a ZBB budget, your goal is to give every dollar a job. You send all of your income to a category and don’t leave any money unassigned. This is a great option for those whose budgets don’t vary much or for those on a low income who need to watch every dollar.

Learn more about the zero-based budget here.

Pay Yourself First budgeting: The pay yourself first budget is similar to the 75/15/10 budget, in that you focus first on your savings goals, then you are free to spend the remaining amount. This budget is ideal if you don’t want to keep track of every dollar, but it can lead to overspending because expenses aren’t being closely monitored.

Learn more about the pay-yourself-first budget here.

50/30/20 Rule: With this budget, you spend 50% of your income on needs, 30% on wants, and you save 20%. It’s a great way to see if your spending on wants is impacting your ability to save. It can also force you to come to terms with what is truly a need and what is a want.

Learn more about the 50/30/20 rule here.

Who is the 75/15/10 budgeting rule best suited for?

Try a 75/15/10 budget if you want to hit your savings goals without tracking every penny. You can use broad spending categories that don’t require you to split Amazon transactions or worry about whether Netflix is a need or a want.

It’s also good for new budgeters, as it focuses on what is truly important: your savings goals. Exactly how much you are spending on coffee or hanging out with friends doesn’t really matter if your bills are paid and you are on track for retirement.

FAQs

How does the 75/15/10 rule treat debt?

Under the 75/15/10 rule, any minimum payments on your debt are considered a bill and included in the 75% portion of the budget. Debt payments you make above the minimum can be viewed as an investment and fall under the 15% budget category, because you are using them to benefit your future and increase your net worth.

What is the 70/20/10 budget?

This budget allocates 70% to spending, 20% to saving, and 10% to charitable giving. It is designed for those who place a high value on charitable giving.

What is the 70/10/10/10 budget?

With this budget, you allocate 70% to spending, 10% to short-term savings, 10% to long-term investments, and 10% to debt repayments. This is a good approach if you don’t consider debt repayment to be bills or savings, or if you want to prioritize it.