Most overspending comes from a bunch of tiny decisions that barely register in the moment. A few dollars here and there, and suddenly that money isn’t going toward saving, investing, or paying down debt anymore.

If you’re struggling to stay within your budget and suspect that small, everyday purchases may be to blame, we’re here to help you spot the biggest offenders. Here are eight expenses you might want to consider cutting back on.

1. Convenience snacks

Ever pick up a candy bar while standing in the checkout line? Or maybe a Diet Coke when you stop for gas? These small purchases add up. They don’t feel like a big deal in the moment, but if you spend $5 per day on small treats, that’s $1,800 a year that could be going to other goals.

If you know you need a little something to get you through the day, plan for it. Packing your lunch is a big win, but tossing in a snack or two can help you avoid impulse purchases.

And no, this doesn’t mean you have to cut out treats forever, but being intentional about your purchases makes them more enjoyable and a lot less expensive.

2. Subscriptions

It feels like everything is a subscription these days. And while each one might be small, they’re sneaky. Especially the annual renewals you forgot you signed up for, or the ones that increase slightly each year.

Scroll through your transactions from the past few months and make a list of your subscriptions. Figure out which ones you’re actually using, and cancel the rest. Even cutting two or three $ 10-per-month subscriptions can add up to meaningful savings over the course of a year.

Trying to reduce the number of streaming services? Consider using your library for access to free TV and movies. Check out your library’s digital library app and see if you can use it to replace some of your streaming apps for free.

3. Food delivery apps

Do you frequently order through DoorDash or Skip The Dishes? Once you add delivery fees and a tip, that $15 meal can quickly become $30. Delivery apps are convenient, but they cost a fortune if you use them regularly.

If you are having trouble discontinuing this service, start by reducing your usage. For example, if you typically order from DoorDash twice a week, go down to once per week. This alone could save you $1,000 per year.

To make it even easier, keep some quick and easy meals on hand. A few frozen pizzas in the freezer might be enough to stop that DoorDash order.

4. Trendy purchases

Social media makes it very easy to buy things you didn’t know you wanted five minutes ago. Between the influencers, the ads, and the limited-time drops, it’s hard not to buy that new trendy item. To make matters worse, these items rarely add any value to our lives.

One helpful rule is to wait 72 hours before buying any discretionary item. This delay provides a “cool off” period, giving you time to decide whether you really want to spend the money without the marketing pressure.

Another option is the “20-use rule.” If you don’t think you’ll use something at least 20 times per year, skip it. Consider borrowing it from a friend or neighbor instead, or look for a used option.

Speaking of used, if you’ve never checked out Facebook Marketplace, you might want to start. You can find almost anything you need for a fraction of the price. You’ll save money, help someone out, and reduce waste all at the same time.

5. Early Upgrades

Upgrading your phone, laptop, or car early costs a lot of money over the long term. If you have an item that is still serving you well, try to make it last as long as possible.

You don’t need to buy a new phone just because Apple or Samsung put out a new model, or your contract is up. You want it, sure, but a few new features aren’t likely to add any measurable improvement to your life.

You definitely don’t need a new car simply because your current one needs repairs. The average new-car payment is $750 per month. That amount of money would cover a huge amount of annual car repairs. Even if you spend an average of $2,000 per year on car repairs, you’ll still be saving $7,000 per year.

6. Amazon

Amazon makes shopping so convenient that it’s easy to buy things we don’t need. They make it so easy that it sometimes doesn’t even feel like you are spending money. With just the push of a button, the item is at your door in two days. It feels more like magic than shopping.

If you love browsing Amazon, but are spending more than you’d like, consider using the “wish list” feature. Create a private wish list and add items you want to buy to it instead of your cart. Then, once a month, batch your purchases. Once per month, review your wish list and buy what you still need.

You might add 30 items to your wish list, but when you review it at the end of the month, you may decide you only actually want two or three. Plus, batching your purchases will help you see exactly how much you are spending.

7. Bank Fees

Bank fees are something you “buy,” but they can quickly drain your bank account. If your bank is charging you fees, it’s time to shop around. Many online banks offer a free checking account with no monthly service fees. If you are being charged other fees, such as overdraft or late fees, you should work towards avoiding these. Using a budget, such as Lunch Money, can help you manage your finances so you don’t incur these fees.

Bank fees are expensive and can pile up fast. For example, if you are paying a $25 monthly maintenance fee, and incur one $35 overdraft fee and one $35 late fee each month (let’s hope you don’t), you’ll spend over $1,000 annually on avoidable fees.

8. Clothing

Clothing is a necessity, but it’s also incredibly easy to overspend on. A new pair of jeans or a new jacket sounds reasonable, but most of the time, our existing clothing is perfectly functional.

Before you shop, take some time to audit what you already own. Before buying a new piece of clothing, ask yourself if it’s something you actually need or just an impulse purchase.

Also, consider using a one-in, one-out approach. Make a rule that if you buy a shirt, you must get rid of a shirt. This will make you think twice about buying something new, and it will keep your closet from getting out of control.

You can also save by buying fewer, higher-quality pieces or shopping secondhand. High-quality items last longer, so they don’t need to be replaced as often. Thrift stores and online resale platforms often offer barely worn clothing at a fraction of retail prices.

How to control your spending with Lunch Money

Need help getting a handle on your daily spending? Lunch Money helps you see exactly how much you are spending on things you don’t really need, especially the purchases you only regret after the fact.

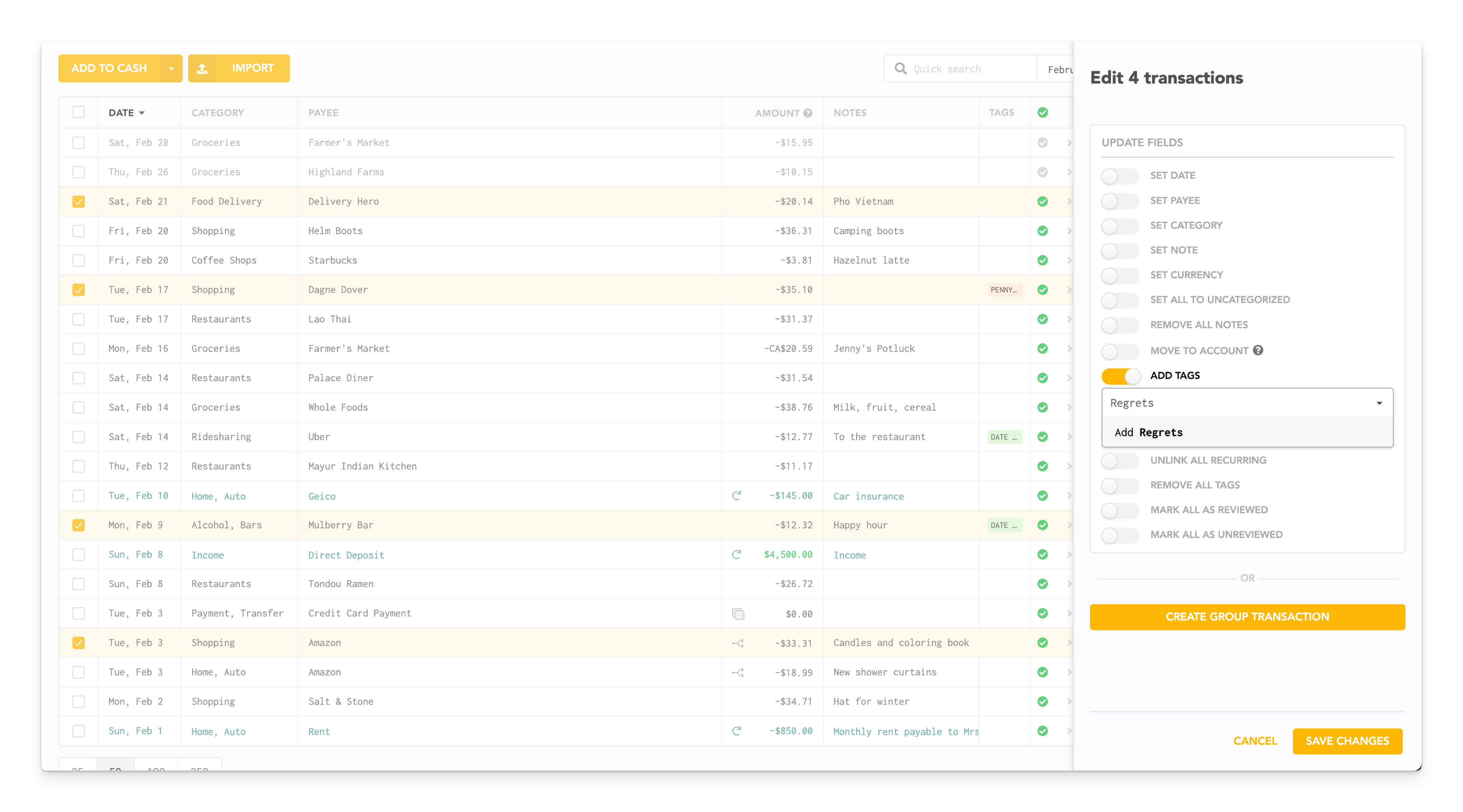

One simple trick? Create tags to apply to purchases you later regret or at least realize were unnecessary.

Start by selecting a few transactions and using bulk edit. From there, you can create a new tag directly on this screen.

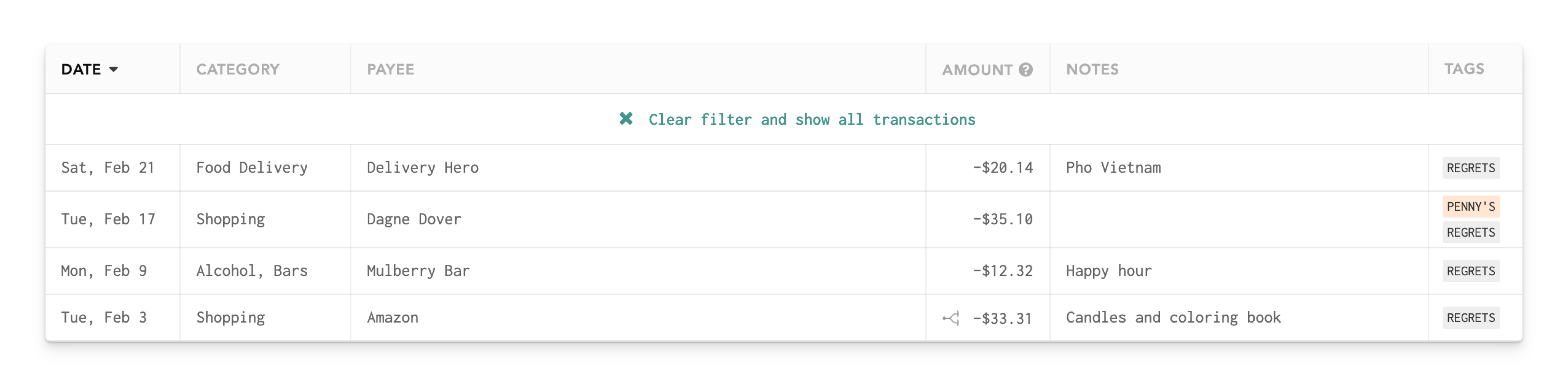

Once you’ve added your tags, you can filter the transactions to see only those with a specific tag.

This will let you see exactly how much money you spend on items that you didn’t really need. Those are dollars you can allocate towards your goals.

Summary

Saving more money in 2026 doesn’t have to mean giving up the things you enjoy. Keep an eye on purchases that aren’t adding value to your life. If a purchase doesn’t meaningfully improve your life, that money might be better spent on other goals, such as debt freedom or retirement.

Tools like Lunch Money make it easier to spot these patterns so you can manage your money with purpose! You can try it for free with a 30-day trial!

For a deeper dive into this topic, check out this video from Jacob, a Lunch Money team member!