Our lives are shaped by habits, and your financial situation is no exception. Creating and sticking to a budget helps you build habits that support your goals and improve your day-to-day life. At its core, budgeting is simply a way to make sure your money is working for you as effectively as possible.

11 Money Habits to Improve Your Finances

Here are some key money habits that can significantly improve your finances over time.

1. Checking your transactions regularly

The best way to stay on top of your spending is to check in on your transactions regularly, ideally a few times a week. It’s incredibly easy to tap your card and forget about it, but those small purchases add up quickly.

Taking a few minutes at the end of the day to see how much you spent will give you a much clearer picture of your finances.

Keeping a close eye on your accounts also helps you spot merchant errors, subscriptions you meant to cancel, or unauthorized transactions.

Lunch Money makes this easy by automatically importing your transactions, so you can see everything in one place. No need to log into multiple bank or credit card accounts. You can quickly categorize transactions, stay on budget, and pull reports when you need them.

2. Naming budget categories in a way that reflects real life, not ideals

Your budget is yours – it doesn’t have to look like anyone else’s. Feel free to name your budget categories however you want. Puns are always popular, and many people enjoy tweaking a song title or lyrics to fit their budget.

For example, someone on Reddit named their fixed expenses “The Bare Necessities,” and someone else named their Emergency Fund “Winter is Coming.” 🤣

Beyond fun names, feel free to categorize your spending however makes sense to you. Again, you don’t have to follow any rules. Want a category just for cheese, or one for buying fun socks?

Go for it! It doesn’t matter. The point of budgeting is to help you meet your long-term goals. If you are doing that, then categorize your spending however you like.

You can make your budget fun with Lunch Money’s custom category names. Personalizing your budget in this way makes budgeting feel a little lighter and less strict.

3. Tagging purchases that don’t fit neatly into one category

Sometimes purchases can fit into more than one category. When this happens, Lunch Money lets you add tags to specific transactions. This allows you to filter transactions and view your spending in different ways.

For example, I use tags when spending for large events that can span several categories, such as a vacation. Sure, there are obvious “travel” expenses, such as flights, hotels, and rental cars. But others are less obvious, such as:

- Gas

- Eating out

- New clothes

- Souvenirs or gifts

Some of the purchases stay in their normal categories, but I tag all trip-related spending with something like “California 26.”

After my trip, I can pull a report showing all transactions with the “California 26” tag, and I can see the total amount spent. I can also revisit that tag later when planning a similar trip to set a realistic budget.

4. Reviewing spending before making changes, not after

A common mistake new budgeters make is to set what they want to spend rather than what they actually spend. Then, when reality doesn’t match the ideal, frustration sets in. If you spend $100 on coffee per month, then set your budget at $100. Setting it at $50 will only lead to frustration.

Even the most experienced budgeters make adjustments to their budget. Doing so doesn’t mean you failed at budgeting. It means you are going with the flow and making your budget work for you.

5. Treating savings like a required expense

The purpose of budgeting is to help you reach your mid- and long-term goals, which usually require saving money. The easiest way to do that is to treat your savings like a bill.

Saving whatever is “left over” at the end of the month rarely works. I’ve budgeted every month for over 25 years, and still make this mistake. If I don’t set a specific savings amount in my budget, it slowly disappears through everyday spending.

6. Planning for “sometimes” expenses ahead of time

If we are honest, very few expenses are true surprises. Cars need repairs. Holidays happen every year. Registration renewals come due.

These aren’t surprises, they’re just “lumpy” expenses.

You can smooth them out by saving a small amount each month. For example, if you estimate that you’ll spend $2,000 on car repairs a year, you should save $166 per month. If you spend $500 on Christmas gifts, then save $42 per month.

Create a budget line item for each expense and allow unused funds to roll over to the next month. Over time, this will create a “sinking fund” you can use when those bills arrive.

7. Making one small adjustment each month instead of a full overhaul

When you start budgeting, you’ll likely notice areas where your spending is higher than expected. But trying to overhaul everything at once usually doesn’t work – it’s too much to adjust.

Think of it like running a marathon. You can’t just get up off the couch and run 26 miles. You have to work your way up to it.

Pick one category or habit to focus on at a time. For example, if you want to spend less on restaurants, start by bringing your lunch to work on Tuesdays and Thursdays. Then bump that up to only going out on Fridays. Then try to limit DoorDash to once a week. Then twice a month, then eliminate it.

Small changes compound over time.

8. Separating the “wants” you value from those you don’t

We all value different things. Some people love trying new restaurants, while others can take it or leave it. Some enjoy the latest designer clothes, while others prefer thrift stores. Some prioritize travel, while others prefer staying home.

The key is spending intentionally, investing more in what you value and less in what you don’t.

Personally, I value food and travel, but not clothes or cars. So I spend as little as possible on clothes and cars so I can spend freely on food and travel.

Someone else might think it’s crazy to spend $100 on a nice dinner while driving a 25-year-old beater, and that’s fine! We all have different values, and our spending should reflect that.

If something excites you or you feel jealous of others for having, it’s likely something you value. Make more room in your budget for those items, and spend less on things you don’t care about.

9. Letting your budget evolve as your life changes

As mentioned, I’ve created a budget every month for the last several decades, and my budget today looks nothing like it did when I started.

Life changes, and your values will too. You might move to a new city, buy a house, or have a baby. You may also value cars when you are young, but then find a love of travel over time… or vice versa.

So it makes sense that your budget will evolve as well. Each month is a fresh start, and you should always create a budget that reflects your current reality.

10. Paying attention to trends instead of individual purchases

No two months are alike. One month, gas costs more; the next month, grocery prices spike. Just make adjustments as you go. But if you notice that a particular category is consistently going over budget, you probably will want to adjust your budget to accommodate more spending.

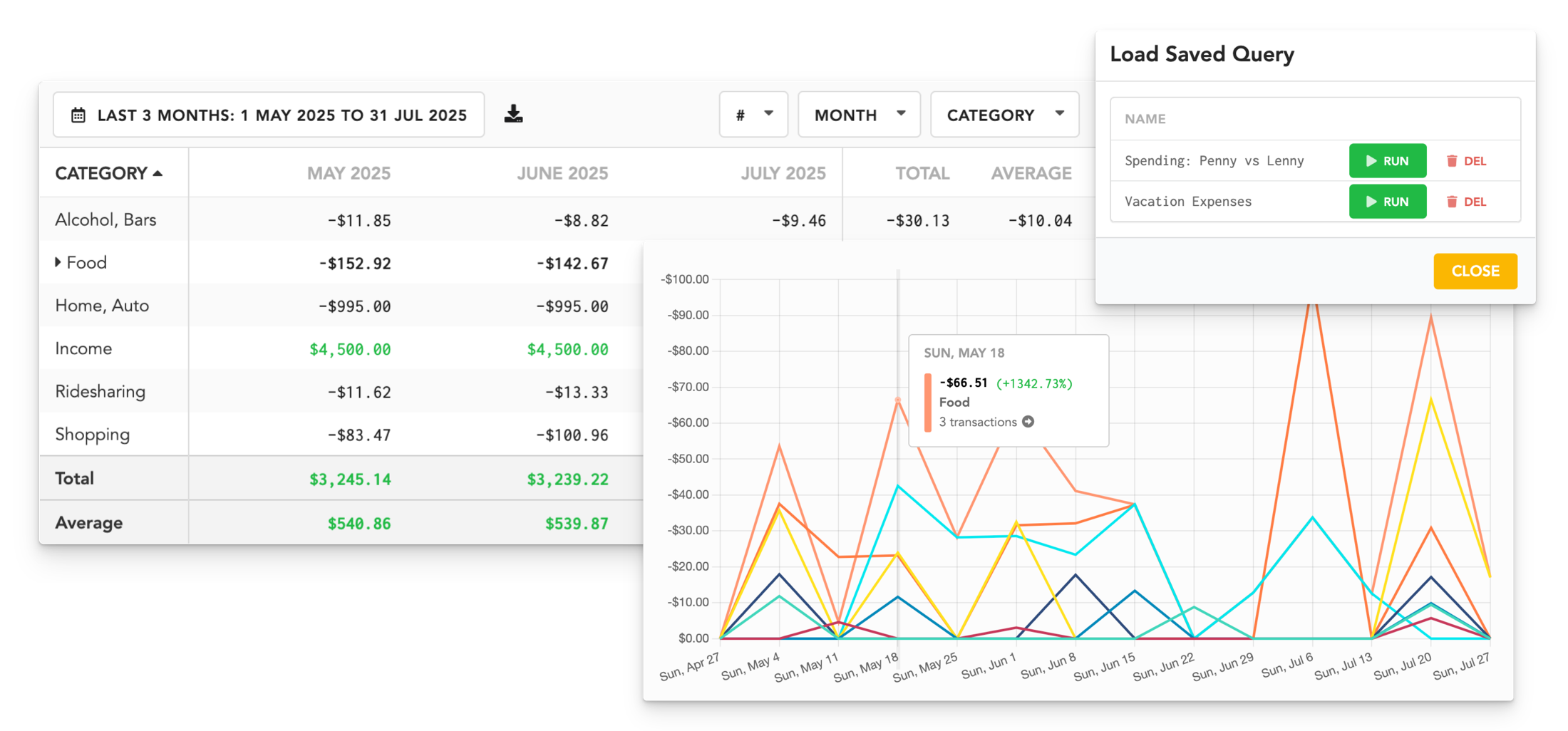

11. Using data to inform decisions, not judge past behavior

Budgeting apps like Lunch Money let you pull reports, view stats, and trends. This is great for identifying areas to reduce spending or for deciding on budget adjustments.

For example, you can pull a report to see how much you spent at a particular retailer or look at several months of spending at once, allowing you to see trends over time. For example, you may notice that you go to restaurants more in the summer and do DoorDash more in the winter.

Or you may notice that you need a bit more of an entertainment budget when the kids are on school break.

These are spending habits that can be difficult to see if you are only looking at one month at a time. But they can really help personalize your budget so it works for you.

Summary

Budgeting is about paying attention and creating a plan that works for your spending and values. If you continue to budget and make adjustments over time, your budget will serve as a launching pad for your net worth.

The key is to be honest about what you actually spend and don’t try to fit your budget or life into someone else’s rules.