Most financial advice skips straight to investing: open a brokerage account, max out your retirement contributions, and start building wealth. While that can be good advice, it doesn’t tell you how much you can safely invest.

Before you can invest, you need to understand your cash flow. That’s where budgeting comes in, and it’s the piece many people miss. Once you know what comes in and what goes out, you’ll know what you have left over. You can then decide how much to save and invest.

Why people struggle to invest consistently

Most people have the discipline to invest, but they aren’t sure how much they can afford to set aside. Here’s what usually gets in the way:

- Your spending is unpredictable. One month you’re under budget; the next, you’ve got a car repair, a birthday dinner, and a vet bill all at once. Periodic expenses make it hard to know how much you can safely move to investments.

- You don’t know your actual surplus. Many people only have a vague idea of how much they earn and spend. But that doesn’t work when you’re trying to invest consistently. You need a clear picture of how much is left over each month.

- Your savings and investment money are mixed together. If your emergency fund, vacation savings, and investment contributions are all sitting in one account, things can get messy fast. It’s best to keep things separated so you always know what’s available to spend and what’s for saving vs. investing.

- Short-term cash flow needs take priority. Investing can feel less urgent than next month’s rent or replacing your broken laptop. If you don’t have a system that accounts for your short-term needs, investing tends to take a back seat.

Budgeting is the missing piece

Budgeting isn’t about restricting yourself. It’s about being intentional with your money.

When you build a budget, you can prioritize the things that matter most to you. That way, when you’ve set aside extra money for important goals (like investing or saving), you’re less likely to spend it impulsively.

Here are a few popular budgeting methods that can help you divide your money between spending, saving, and investing:

| Budgeting Method | How It Works | Best For |

|---|---|---|

| 50/30/20 | 50% to needs, 30% to wants, 20% to savings and investing | People who want a simple system with clear limits |

| Zero-based budgeting | Every dollar gets assigned a purpose until you hit zero | People who want to optimize each paycheck |

| Pay yourself first | Savings and investments come out first, and you spend what’s left | People who struggle to save consistently |

No method is better than another — the best one is whichever you’ll actually stick to.

How Lunch Money helps you build the right system

When it comes to investing vs. saving, building a system that keeps you consistent is what matters most. Here’s how Lunch Money can help:

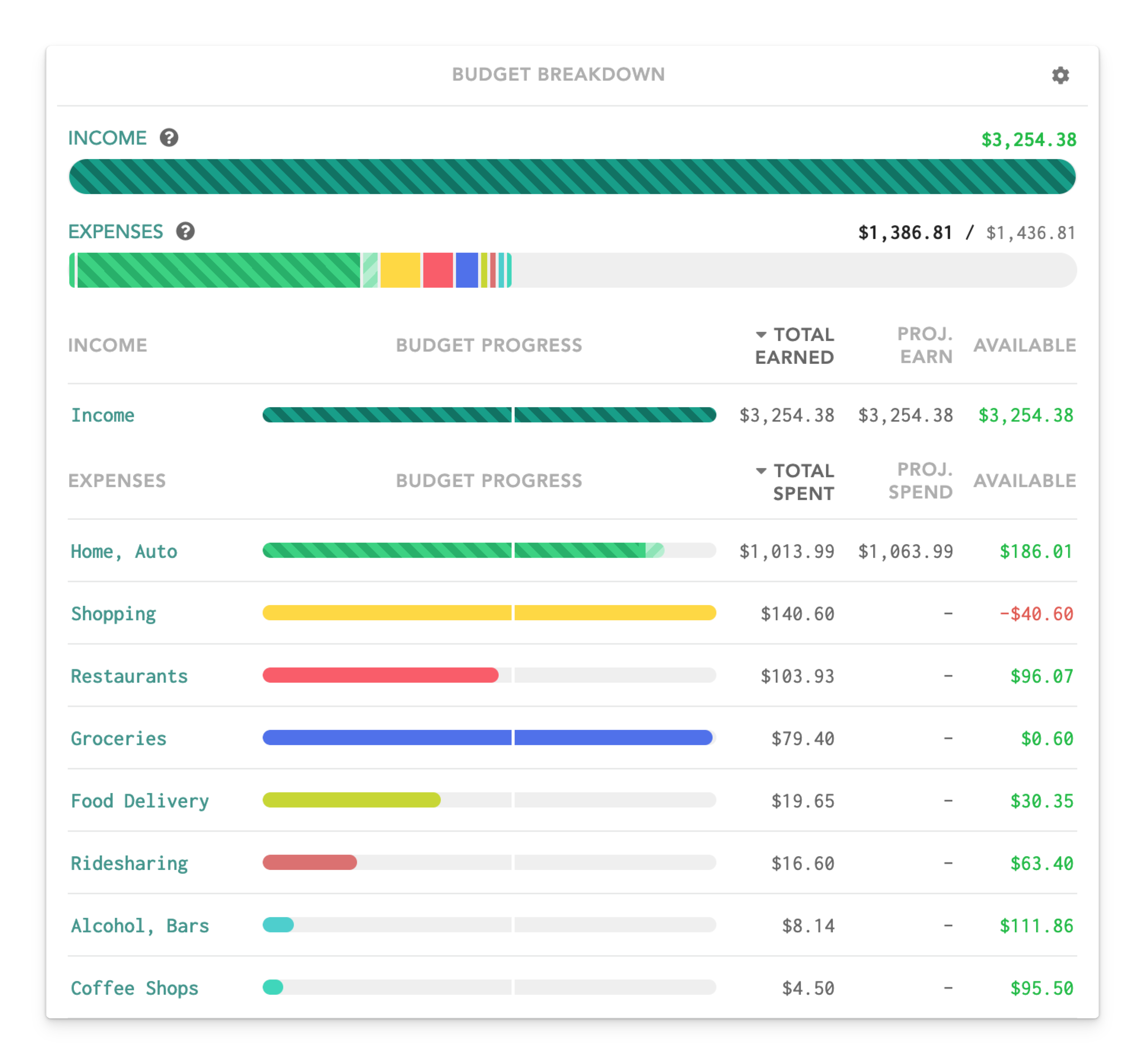

See exactly what you have leftover for saving and investing

Lunch Money automatically subtracts your expenses from your income to show you what’s left over. That number is your monthly surplus, one of the most important figures in your budget.

When you see exactly how much money you have after paying all your expenses, you can put that money to work by transferring it to savings or your investment account.

Separate your short-term and long-term goals

Lunch Money lets you create budget category groups with subcategories under each one. This feature gives you a clear distinction between your funds and lets you separate your short and long-term goals.

For example, your savings group might include an emergency fund, vacation fund, or new car fund. Meanwhile, your Investing group might have subcategories for retirement contributions or a taxable brokerage account.

Track your investment contributions

Although Lunch Money doesn’t monitor your investment portfolio’s performance, you can use it to track how much you’re contributing each month. You can add your investment account transfers as a budget category, so you always know if you’re hitting your targets.

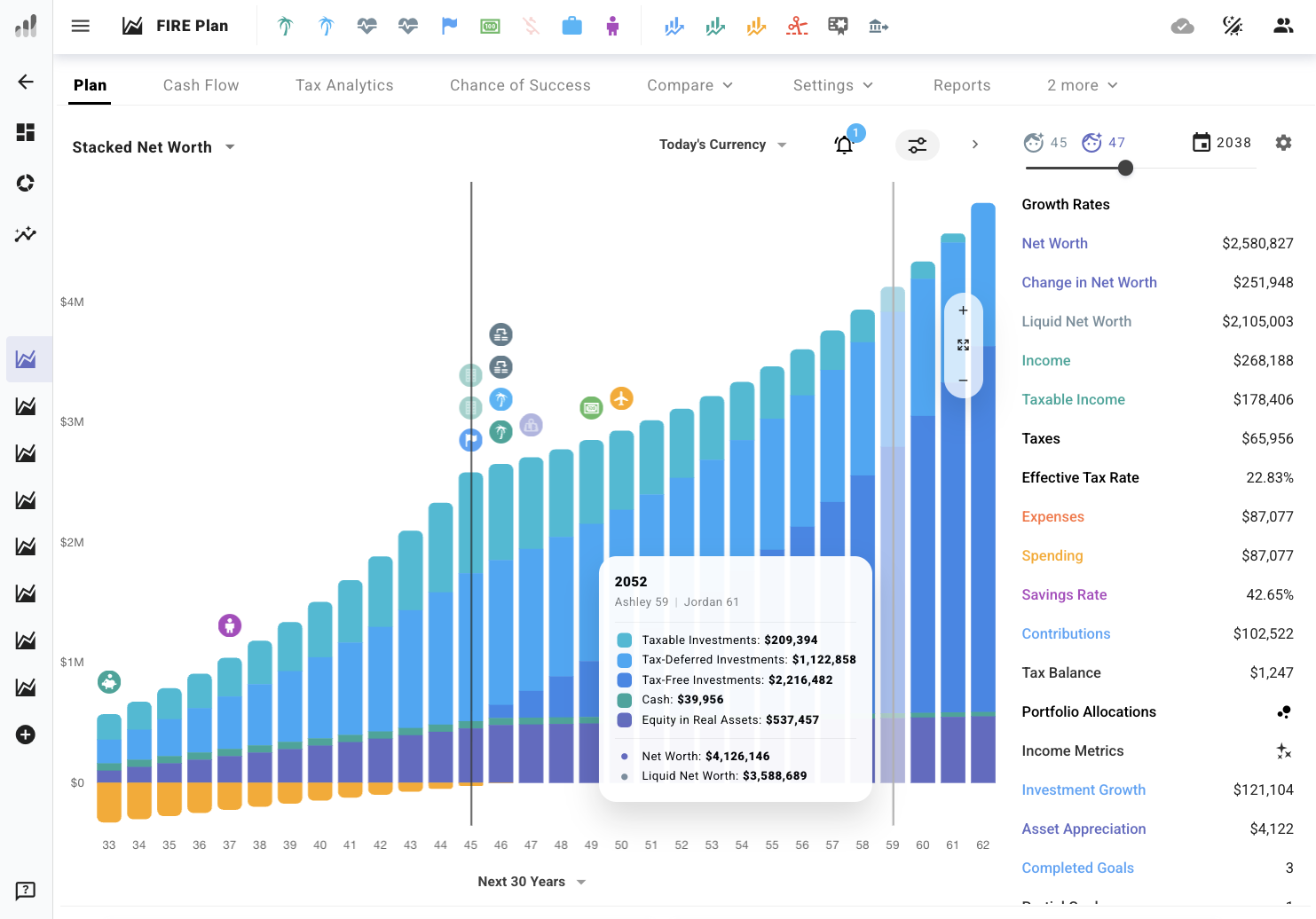

Lunch Money has also partnered with ProjectionLab, a long-term financial planning tool that connects directly to your Lunch Money data through a free Chrome extension. Together, they turn your budgeting numbers into real future projections, including retirement timelines, tax estimates, and “what if” scenarios.

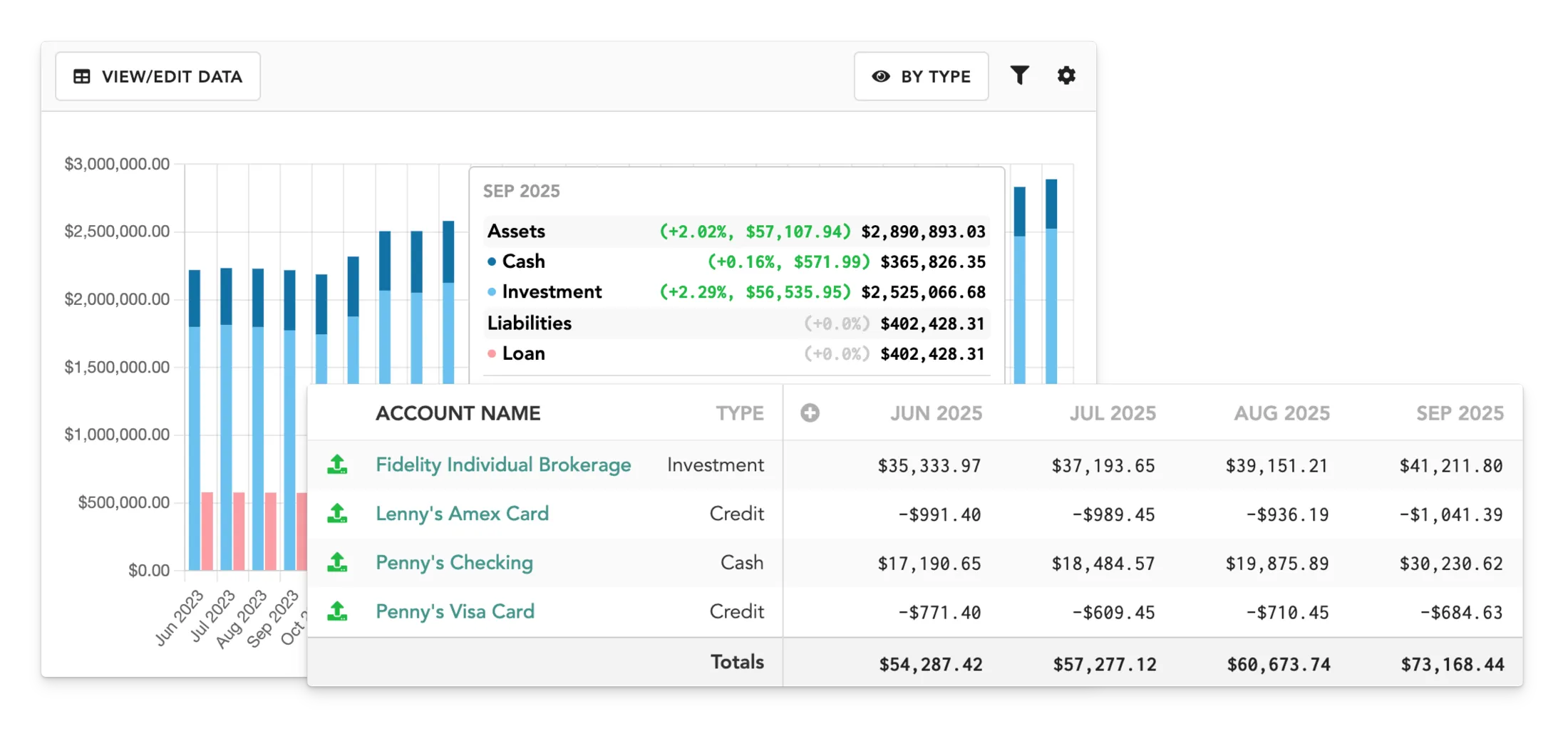

Monitor your net worth

Your net worth is the total value of everything you own (your assets) minus your liabilities, such as a mortgage, credit card balance, or student loan debt. Seeing your net worth can give you a clear picture of your financial health and areas for improvement.

Lunch Money automatically syncs your accounts — including bank balances, credit cards, and loans — and provides you with an up-to-date snapshot of your net worth, in a simple chart. This allows you to visualize how your assets and liabilities have changed over time.

A simple system for saving and investing

Now that you understand your cash flow and how Lunch Money can help you save and invest, here are some ways you can put it into practice:

- Create a budget with Lunch Money: Before you can start saving and investing, you need to know where your money’s actually going. Sync your accounts in Lunch Money, categorize your income and expenses, and set limits on different spending areas.

- Track your spending: Once you’ve created your budget, monitor your spending to see where it needs adjusting. Maybe you need more breathing room for groceries, but could cut back on restaurants.

- Use your excess funds to build an emergency fund: Before you invest, make sure you have a financial cushion. Even a small buffer, like $1,000 or one month of expenses, can keep unexpected costs from throwing off your plan.

- Identify your surplus and automate your transfers: Once you know your monthly surplus (thanks to all that tracking), you should put that money to work. Set up automatic contributions to your savings or investment account (even a small amount), so it happens without even thinking about it.

Summary

Saving and investing can take a backseat when you don’t know how much you can comfortably set aside. Short-term needs often take precedence, especially when your expenses are unpredictable.

Lunch Money lets you see the full picture of your finances, making it easier to find your surplus and decide between saving and investing. If you want to see it in action, you can try Lunch Money for 30 days and start building wealth today.