Buying a car is one of the biggest financial decisions you’ll make, and it’s about a lot more than the sticker price. Beyond the car itself, you’ll need to factor in fuel, insurance, and maintenance costs.

A good place to start is to figure out what you can realistically afford. Here’s how you can use the 20-4-10 rule (along with smart budgeting) to figure out what you can truly afford.

1. Understand What You Can Afford

Before you start to save, it’s a good idea to step back and look at the big picture. According to Lending Tree, the average new car costs about $50,000, while the average used car is about half that amount. Those are huge numbers that can significantly impact your finances. So it’s important to take a moment and consider what you can actually afford.

Use the 20-4-10 Rule When Buying a Car

The 20-4-10 rule is a simple guideline for car buying when financing:

- 20% down

- 4-year loan

- No more than 10% of take-home pay on total transportation costs

Here’s how it works:

20% down payment: Putting 20% down helps reduce the amount you borrow and the interest you’ll pay. For example, on a $25,000 car, that means a $5,000 down payment. Remember that taxes and registration are usually on top of this amount.

4-year loan term: Dealers often encourage longer loan terms because they lower the monthly payment, making it easier for them to sell you a more expensive vehicle and charge more interest on the loan.

But while a lower monthly payment can make a car feel more affordable, it will almost always cost more in the long run.

For example, let’s take a $20,000 loan at 6% APR:

- 4 years: $469.70/month

- 7 years: $292.17/month

The longer loan saves you about $177 per month, but you’ll pay nearly $2,000 more in interest overall and stay in debt for three extra years.

10% of take-home pay: The “10” in 20-4-10 is a reminder to keep all transportation costs, including your loan payment, gas or electricity, insurance, repairs, and maintenance, under 10% of your take-home pay.

Estimate Other Expenses

Your monthly payment is only part of the story. On average, the cost to own a car (outside of the payment) is about $4,500 per year, according to Lending Tree. But of course, your mileage may vary, so it’s a good idea to run the numbers for yourself.

Gas/ Electricity

If you already have a car, you may already have an idea of what you are spending on gas or electricity. If you are switching vehicle types, say, going from a gas to an electric, you’ll want to do some research.

The national average for a gallon of gas is about $3.20. If you know about how many miles per gallon your car gets, and about how much you drive per month, then you’ll be able to figure out your monthly fuel costs.

For example, if your car gets 20 miles per gallon and you drive 1,000 miles per month, then you’ll need 50 gallons of gas. At $3.20 per gallon, that will cost $160 per month.

If your car is electric, you’ll need to know your cost per kilowatt-hour (kWh). The average cost per kWh is 17.78 cents. You’ll also need to know your car’s consumption, which will be listed as kWh per 100 miles. Then you’ll need to know how much you drive.

For example, if your car uses 30 kWh per 100 miles and you drive about 1,000 miles, then you’ll need 300 kWh per month. At 17.47 cents per kWh, this will cost you about $57.65 per month.

Insurance

Before finalizing your car purchase, call your car insurance company and get a quote for the vehicle you want to buy. If you already have a specific car picked out, your quote will likely be pretty close to what you end up paying. If you only have the make and model, you’ll receive a general quote; it won’t be exact.

Repairs and Maintenance

Search online and see what average repair costs are for the type of car you are considering. Consumer Reports recently analyzed major car companies and the cost of maintaining their vehicles over a 10-year period.

Tesla came in at only $5,050, while Land Rover costs $17,450 to maintain for 10 years. While the exact costs for your car will vary, these estimates will give you a good idea of what to budget for.

Other Costs

There may be additional costs associated with car ownership, such as parking or tolls.

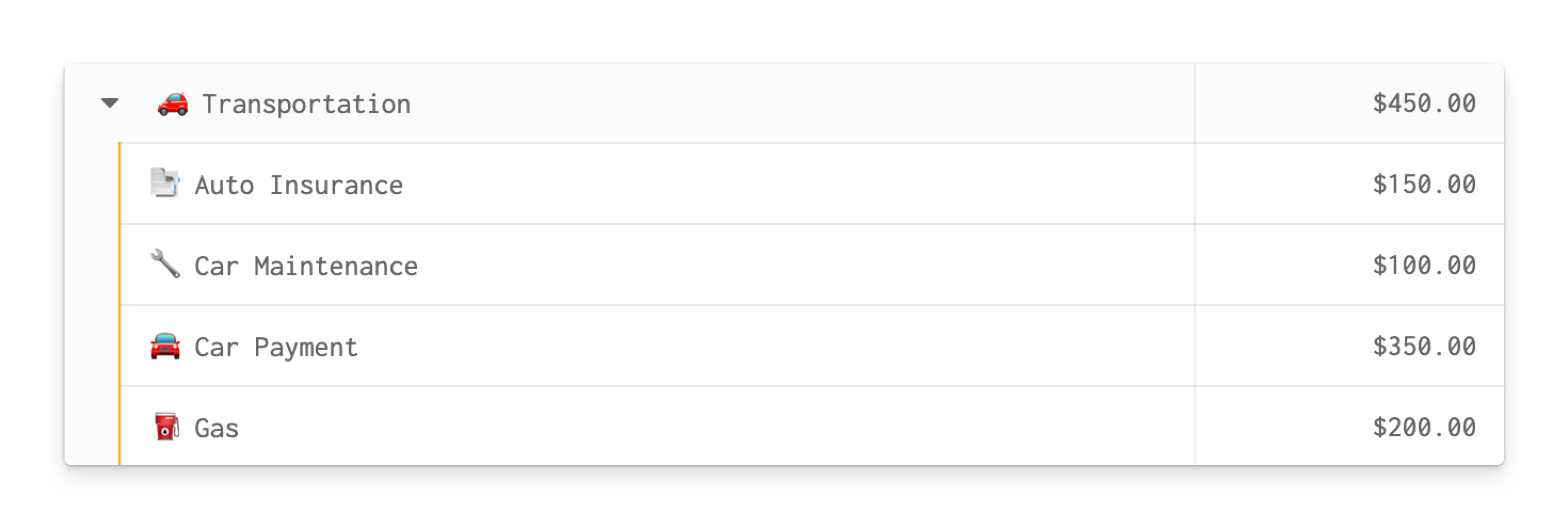

Create line items in your budget for each of these costs to track your spending. You can create a category group to see exactly what you are spending on transportation.

Here’s an example of an $ 800-per-month transportation budget. As you can see, it adds up quickly!

2. Review Your Budget

Start by calculating 10% of your take-home pay and decide whether that feels reasonable for transportation. Rules like the 20-4-10 rule are helpful guidelines, not hard limits.

Once you land on a monthly number that works for you, plug in estimated costs for gas, insurance, and maintenance. Whatever’s left is what you can comfortably afford for a car payment.

For example, an $800 transportation budget might include the following costs:

- $200 for gas

- $150 for insurance

- $100 for maintenance

That leaves $350 per month for a car payment. At 6% APR over four years, that supports a loan of roughly $15,000.

Paying Cash

Of course, you don’t have to borrow money to buy a car; you can pay cash, but the budget doesn’t change that much. You’ll still want to set aside a monthly amount to build a fund for the car purchase.

Instead of “car payment,” you could label your budget category something else, perhaps “car savings.”

If you can afford a $350 car payment, then you can afford to save $350. If you set aside $350 per month for four years in a high-yield savings account earning 4%, you would have over $18,000.

Saving up the money first allows you to get a slightly nicer car for the same cost over the same period. It’s the difference between paying interest and earning interest over those four years.

3. Start Saving

Exactly how you save for a car is up to you. If this is a purchase you aren’t making for a

while, you may want to open a savings account specifically for this purpose. Or you can create a line item in your budget and keep the money in your checking account. This will work well if you plan to make the purchase soon.

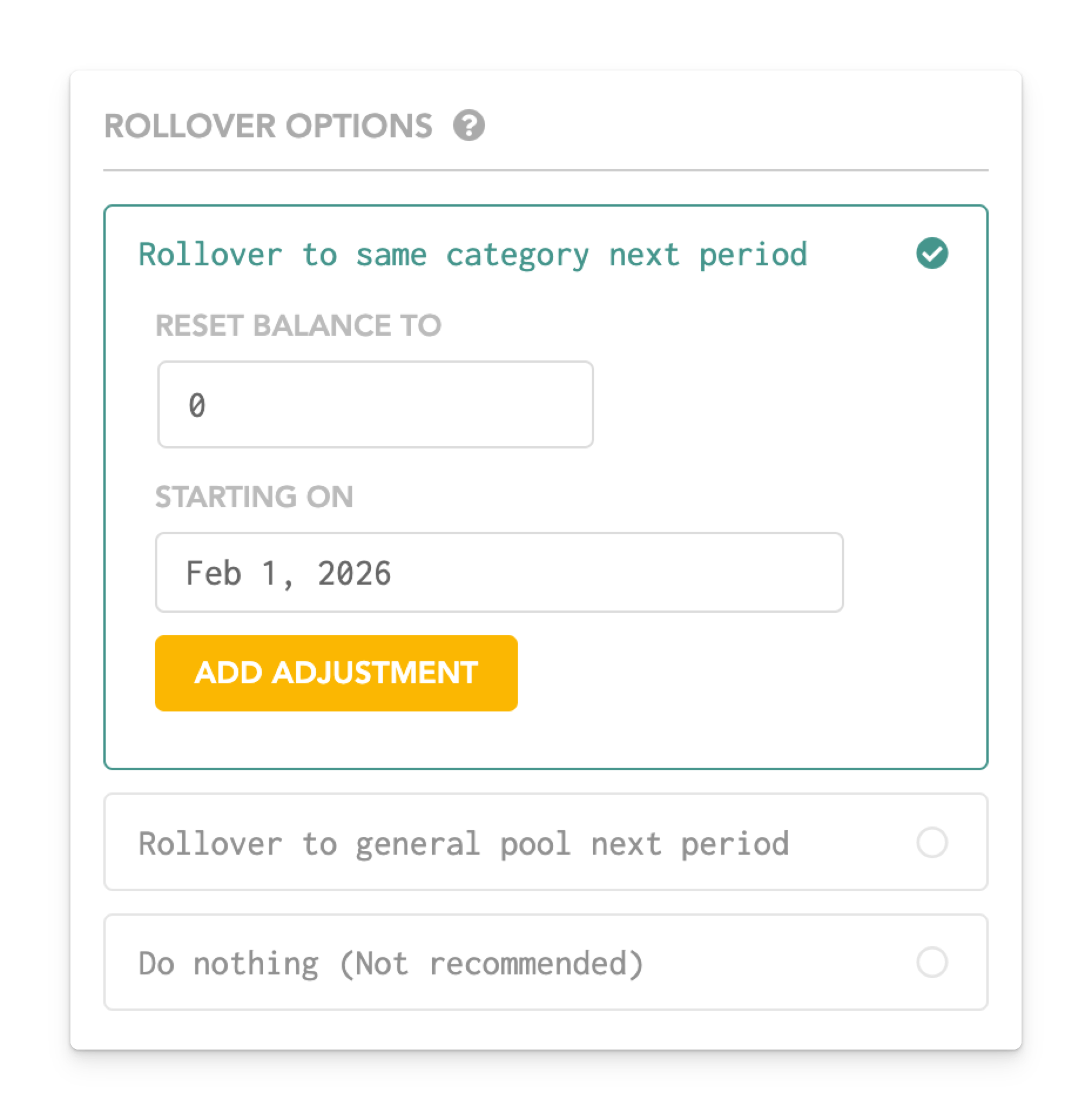

If you are creating a line item, set the category to roll over the unspent money into the same category at the end of the month. The fund will increase each month, and you’ll be able to see exactly how much you have saved.

You can do this in the category details:

4. Prepare for the Future

If you’ve taken out a loan to purchase your car, pay it off as quickly as you can to reduce the amount of interest you have to pay.

Once the loan is paid off, try to continue making the monthly payment into a savings account so you are prepared for your next car purchase.

Saving more money will allow you to either:

- Buy a nicer car for the same monthly cost, or

- Spend less per month on the same quality car

The less you borrow, the less interest you pay, which means more flexibility with your money.

Final Thoughts

Saving for a car doesn’t have to feel overwhelming, as long as you break it into clear, manageable steps. Start by understanding what you can truly afford, then plan for the total cost of ownership. If you’d like, you can follow the 20-4-10 rule and use a tool like Lunch Money as you plan.

By being intentional about saving, you will put yourself in control of your car purchase instead of being a slave to the monthly payment. Remember, whether you finance or pay cash for your car, your goal should be the same: buy the car that fits your life without putting pressure on your overall budget. By planning now, you’ll save thousands and have less stress down the road (no pun intended). 😊