Saving for a house can feel overwhelming, especially when you hear you need a 20% down payment. That’s a big number!

The good news? First-time homebuyers have more options than ever. By combining smart saving strategies, realistic goals, and the right budgeting tools, homeownership may be closer than you think.

Let’s break it down.

Set a clear savings goal

You’ve probably heard that you should save 20% of the purchase price for a down payment. While that’s a reasonable guideline, it’s not always realistic, especially if you are a first-time homebuyer.

According to Zillow, the average home price in the U.S. is over $350,000. That means you would need to save over $70,000 just for the down payment. And that’s before factoring in other costs like closing fees and moving expenses.

If you are a first-time homebuyer in the U.S., you can get a home loan that allows you to buy with as little as 3.5% down (5% down in Canada). There are also programs for those with modest incomes that allow for lower down payments. It’s always worth discussing your options with a lender to see what you qualify for.

For example, if you qualify for a loan that requires 3.5% down, you would only need to put down around $12,700 for the average-priced home. Compare that to $70,000, and you can see how these programs bring home ownership within reach for many.

Of course, the down payment isn’t the only cost you’ll need to plan for.

Zillow reports that closing costs typically range from 2% and 5% of the loan amount. On a $350,000 mortgage, that could mean paying between $7,000 and $17,500.

If we assume a down payment of around $13,000 and closing costs of around $12,000, that leaves you with a savings goal of about $25,000.

That number may still feel big, but it’s far more manageable than $70,000.

Open a high-yield savings account

Once you’re ready to start saving, open a high-yield savings account dedicated to your down payment.

One simple trick that helps many people: keep this account at a different bank than your checking account. When the money isn’t sitting right beside your everyday spending, it’s easier to avoid dipping into it.

Out of sight, out of mind.

It can also help to give your account a clear name, such as “House Fund” or something similar. Seeing that label every time you check your balance can be surprisingly motivating.

High-yield savings accounts also pay higher interest rates than traditional savings accounts, allowing your savings to grow a little faster over time. These accounts are often offered by online-only banks, although traditional banks are starting to get on board.

Pause other big spending goals

Saving for a down payment is a major financial goal. While you are working toward it, it often helps to pause spending on other large goals, such as vacations or car upgrades.

Small splurges that make life enjoyable are still perfectly fine, but trying to save for multiple big purchases at once can slow your progress.

When your focus is split, it can seem like you’ll never achieve your homeownership goals. Stay laser focused, and you’ll be surprised at how quickly you can hit your savings goal.

Pause unnecessary spending

Along with pausing big purchases, it’s worth taking a close look at your budget and identifying smaller expenses that you could redirect toward your home fund.

Individually, these expenses might not seem like much. But over time, multiple small purchases can add up to a significant amount.

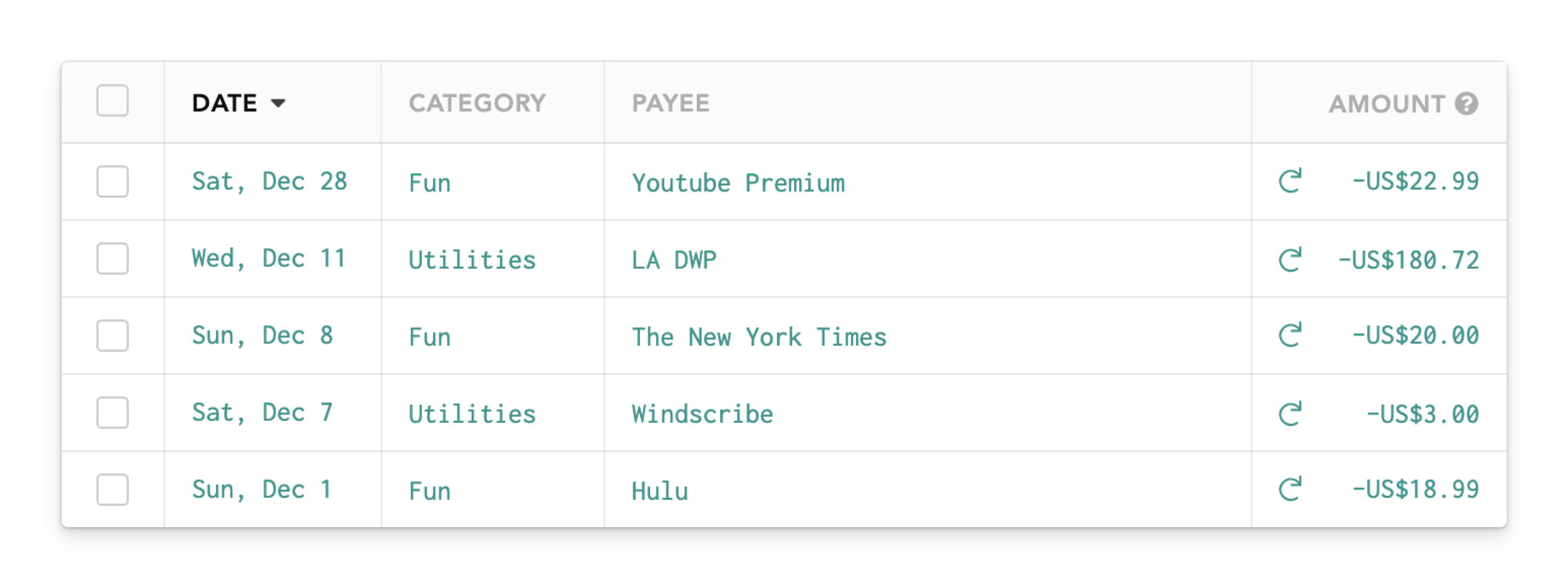

Start by reviewing your subscriptions. Are there any services you’re not getting enough value from?

You don’t have to cancel Disney+ forever, but if it’s something you could pause for a year or two while you save, the extra cash can make a big difference.

It’s also worth reviewing your daily spending habits. Even if you can’t cut something entirely, is there a way to spend less? For example, switching to a lower-priced plan for a service you use regularly.

Remember, these changes aren’t permanent. They’re temporary adjustments that will help you free up some cash so you can reach your goal faster.

This is where Lunch Money can really help.

With Lunch Money, you can see exactly where your money is going, making it much easier to spot areas where you can cut back without relying on guesswork.

Start a side hustle

Earning additional income can give your savings a serious boost. Even a few hundred extra dollars per month can significantly speed up your progress toward a down payment.

If you take on a side hustle, the key is to send that extra income directly to your down payment fund. Try not to increase your lifestyle with the additional money.

If the extra income goes directly toward your savings goal, you’ll build your down payment much faster, and you won’t have to rely on that side hustle income long term.

Create a visual goal and set celebration points

You’ve probably seen those big thermometers that charities use to display their progress towards fundraising goals.

There’s a reason they do that. It’s very motivating for people to see progress visually.

You can do this for yourself! Print out a simple thermometer on a piece of paper and put it where you will see it, like on your fridge. Every time you deposit money into your down payment account, color in a little more of the progress bar.

This helps to keep your goal top of mind, while allowing you to see how far you’ve come and how much further you still need to go.

You can also set milestones and celebration activities along the way.

For example, you might decide to go to dinner when you’ve reached the halfway point of your goal. Or buy a sweet treat each time you save another $1,000.

How Lunch Money can help you save for a house

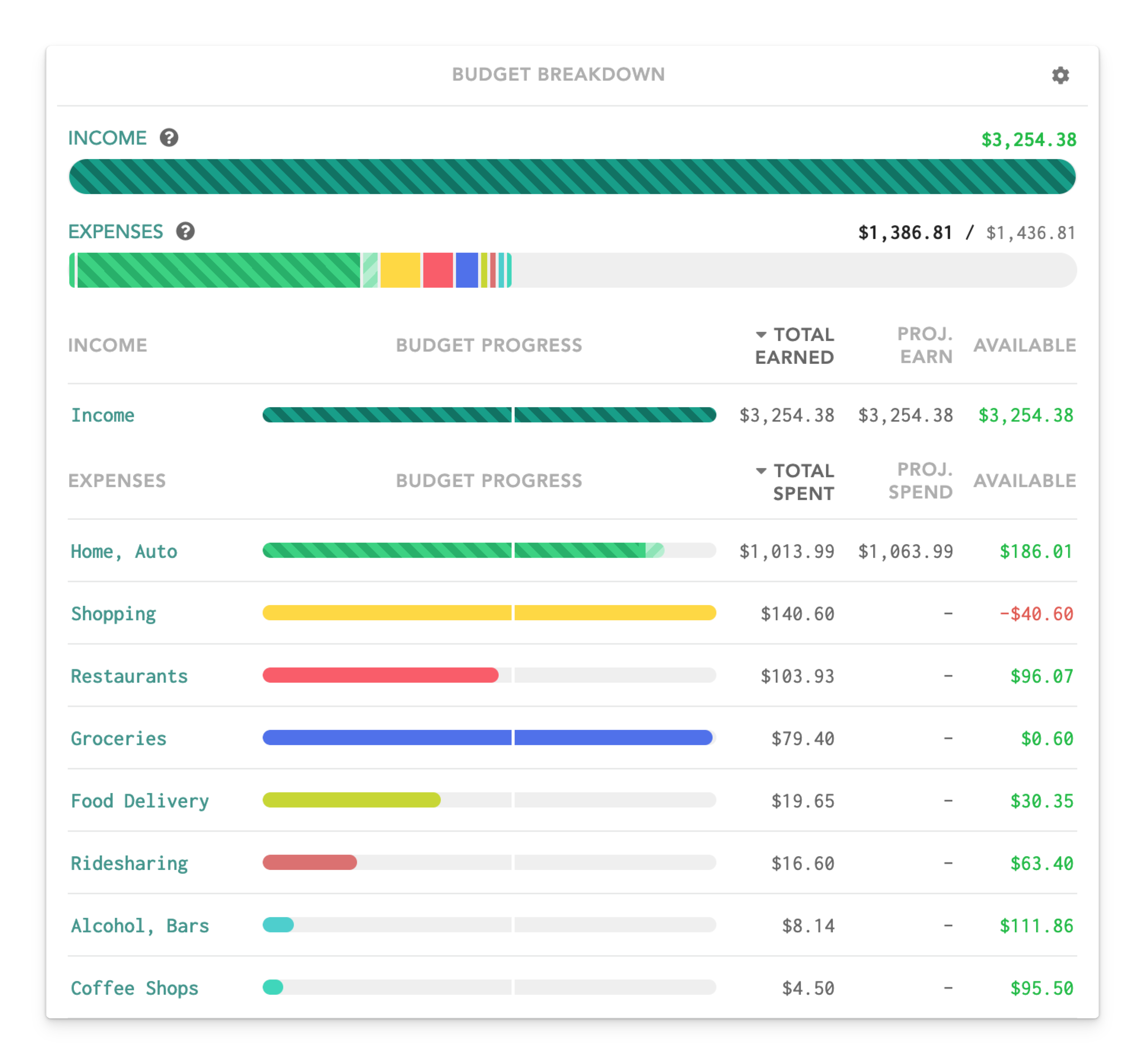

When you create your budget in Lunch Money, it automatically pulls in transactions from your connected banking accounts. You can then categorize those transactions accordingly. Once all your transactions are assigned to a category, you’ll be able to see exactly where you spend your money and make changes to the budget.

Summary

This guide was inspired by this YouTube video, from our very own Jacob Wade. In it, he walks through practical ways to save for a house faster, even if a 20% down payment feels out of reach. Tools like Lunch Money make it easier to track your spending, spot opportunities to save, and stay focused on your goal. If you’d like to try it yourself, you can start with a 30-day free trial of Lunch Money!