In the summer of 2023, amidst rising inflation and economic uncertainty, I decided to make a significant change to Lunch Money’s pricing structure. Instead of raising prices (which is what every other company was doing), we introduced a pay-what-you-want pricing model for annual plans, starting from $40 up to $150 per year.

Our newest (and current) annual pricing plan!

Prior to the change, we were offering Lunch Money for US$100 per year. Our pricing in 2024, 5 years into running our business, would essentially drop down to 2019 levels at the lowest. And though we send out thank you gifts to our highest-tier subscribers, those paying $40 a year have access to exactly the same feature set.

Roughly a year after this decision, our user growth has not slowed, revenue has nearly doubled and churn and trial conversion rates are healthier than ever.

Let’s go back to the beginning…

Though pricing is notoriously difficult to get right, the upside is that we can iterate quickly with a SaaS product.

In the beginning, I launched the app in Aug 2019 at $3 per month and $29 per year. Despite only launching with 3 features (transactions, budgeting and recurring items), I received feedback that our pricing was too low! Over the next few months, I increased our pricing by a dollar a month every time a new major feature was launched. CSV imports and a developer API justified the price jump to $5 per month. Next, the rules engine and query tool increased the monthly price by another dollar each.

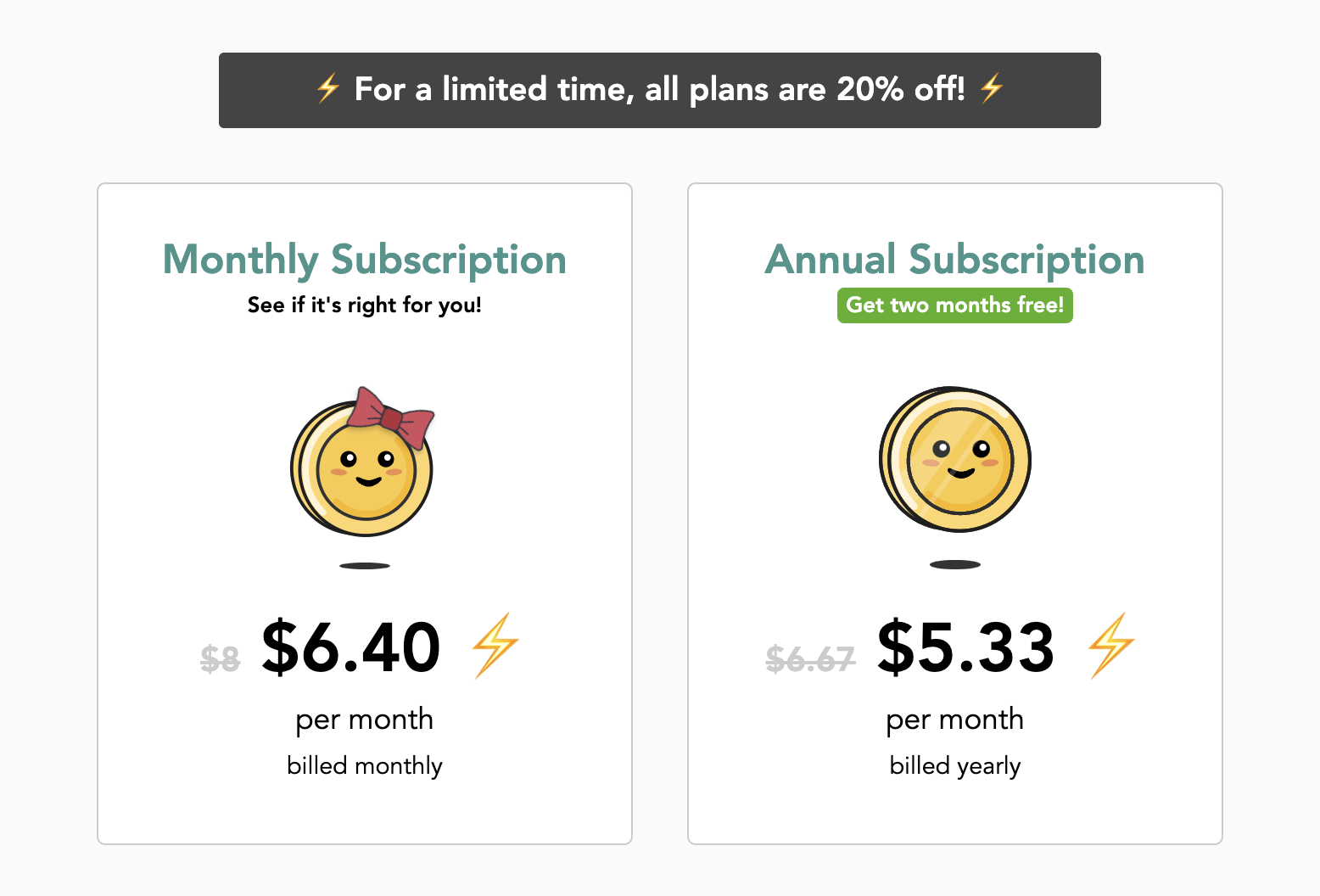

Our old pricing plan – $8 per month was clearly too much so we added a lifetime 20% discount.

We basically raised our prices every month until we started to see a slowdown in signups and conversions. That happened at $8 per month in March 2020. Because I didn’t want to lower prices back down, I offered a lifetime 20% discount, effectively changing the price to $6.40 per month. This discount stuck for about 1 year, and in Jan 2021, I made our final price increase to $10 per month or $100 per year* with a first year discount of 50%.

By this point, our Stripe product catalog was looking like a mess but folks seemed happy to be paying what they were paying. I should mention that the price increases only affected new subscribers. We have never forced early adopters and loyal existing customers into higher pricing tiers, and we don’t plan to.

* We also offered pricing plans in EUR and CAD at slightly different prices.

It never hurts to ask!

At the time, $10 per month or $100 per year was on the high end for a personal finance management app, especially when Mint was still around and offering their product for free. My thinking was that we were offering a premium product at a high price and in the end, we would need fewer customers to sustain our revenue growth.

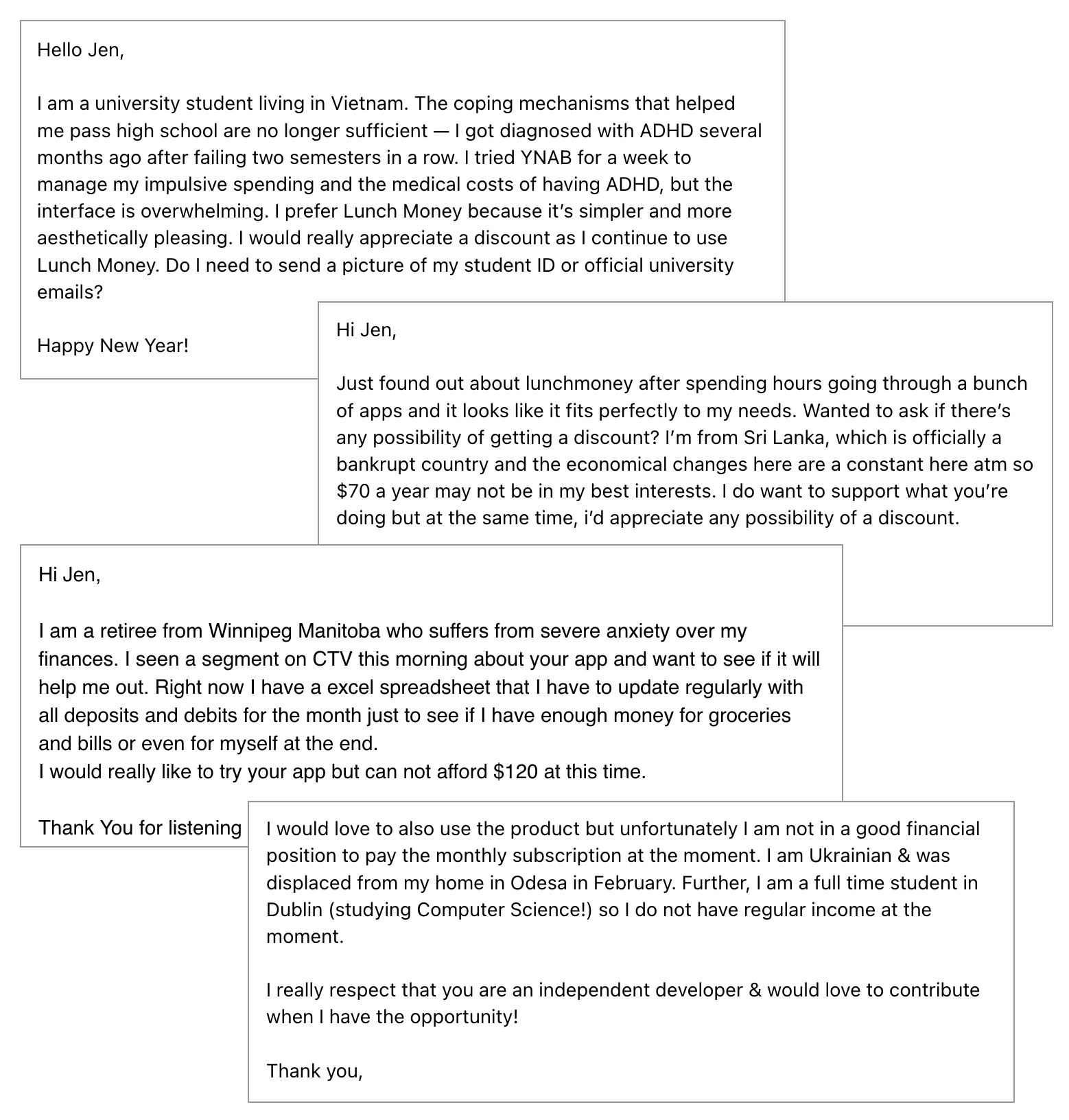

With the awareness that our price point was unattainable for some, I decided to give folks the option to email in for a discount on our Pricing page. I had no idea how many would even see this since it was below the fold, but over the next few months, I received dozens of requests from folks sharing stories on how Lunch Money has or could help them in their financial journeys. It was the first time my eyes opened up to just how much impact we could have on people from all different walks of life.

Really touching requests for discounts I received over the years.

Thought Process and Justification

Fast forward a year and a half later, I had a major traumatic event that changed my philosophy on running Lunch Money. I go more into detail here but in short, I rearranged my priorities and decided that my original goal of being a premium and pricy product to achieve higher and higher revenue status no longer aligned with my personal values or where I wanted to take Lunch Money.

I felt it would be much more satisfying and appealing to my passion to shift our mindset to expanding access to as many people as possible.

I was inspired by a podcaster (David Pakman, for those curious) for the idea of a sliding pricing scale which would simultaneously welcome users from different economic backgrounds and reward folks who were willing to pay more. As humans, we are masters of rationalization, so here were my main reasons:

1. This could lead to higher retention and lower churn

You’ll be able to retain a user for longer if they feel they’re getting a great deal! Someone who is paying $100 per year for a product in which they are just passively tracking their finances or parking their data may churn by the end of year 1, but if that same person was able to pay $40 per year, they’ll likely end up sticking around for much longer. We’re in it for the long haul, not short-term spikes in quarterly profits.

2. We would be a differentiator in the business world

I started my career in Silicon Valley where every entrepreneur is pushed down the same path of raising funding, building a team quickly, and burning out while staying under the thumb of investors and board members that just want them to maximize returns.

With our roots in building in public, launching Lunch Money as a bootstrapped company was my way of making a statement that there are other paths to entrepreneurship, especially for those of us who don’t do very well in high-pressure situations and don’t necessarily want to kick off a business with millions in debt to investors.

As a consumer, I’m also constantly frustrated by sneaky business practices, hidden fees and unethical, but legal tactics to get more money from me. I love utilizing Lunch Money to be the change I want to see in the way companies do business.

3. We could build a bigger community and reach more people worldwide

You’ll want to check out this blog post to see why this matters to me on a deeper, personal level.

4. It would help us remove some billing tech debt

It’s good to have a bias for keeping things simple. This would allow us to clean up our Stripe product catalog and remove the need for discounts and coupons.

5. It would be a fun experiment

As a bootstrapped and profitable company, it’s genuinely fun to be able to run experiments like this and not have to worry about the immediate impact on our revenue or growth numbers. My previous employers would never…

In the end, what happened?

When I updated our pricing model, I initially did very little marketing around it, and only new subscribers would be aware of it. Existing subscribers could see it from the billing page.

A few months later, Mint, the largest personal financial management app shut down. This was a blessing for us since we got a ton of new users. But it also muddies the waters and makes it difficult for us to track the effects of our pricing change on user and revenue growth.

One could also postulate that we were able to convert many post-Mint users due to our lower pricing compared to competitors. Since ex-Mint users were used to a free product, they would naturally feel less friction with paying $40 per year versus the $90 to $120 per year our competitors were offering.

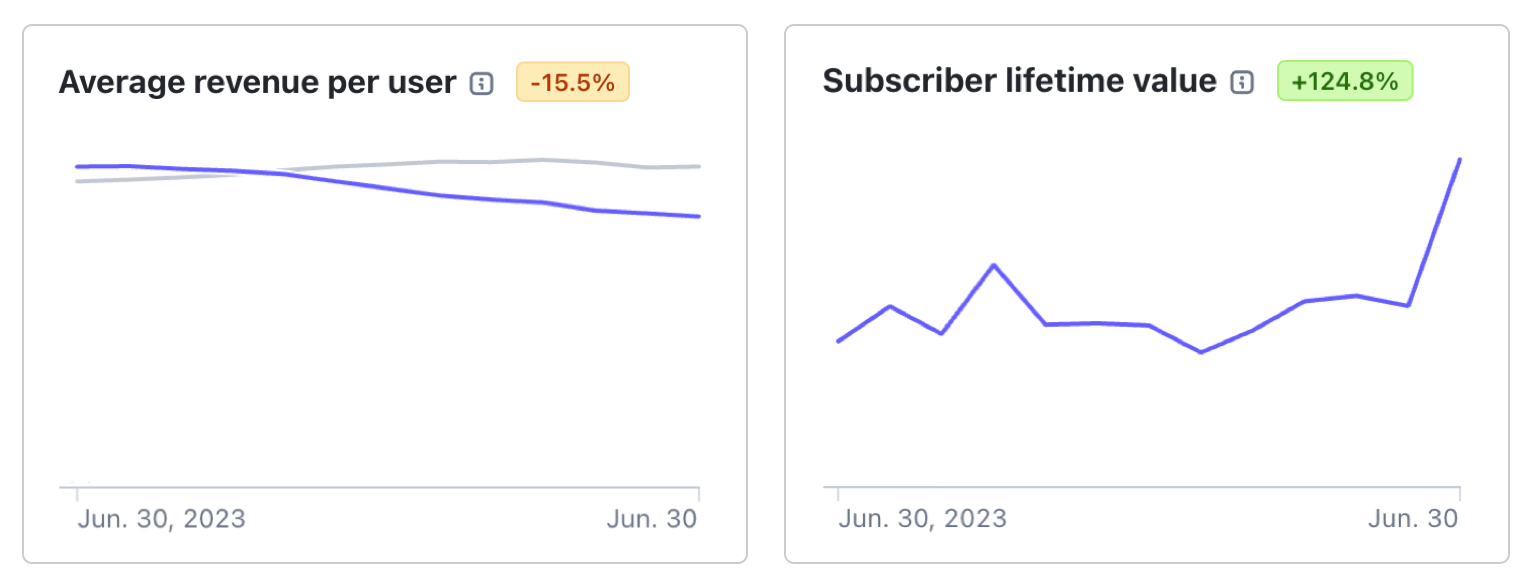

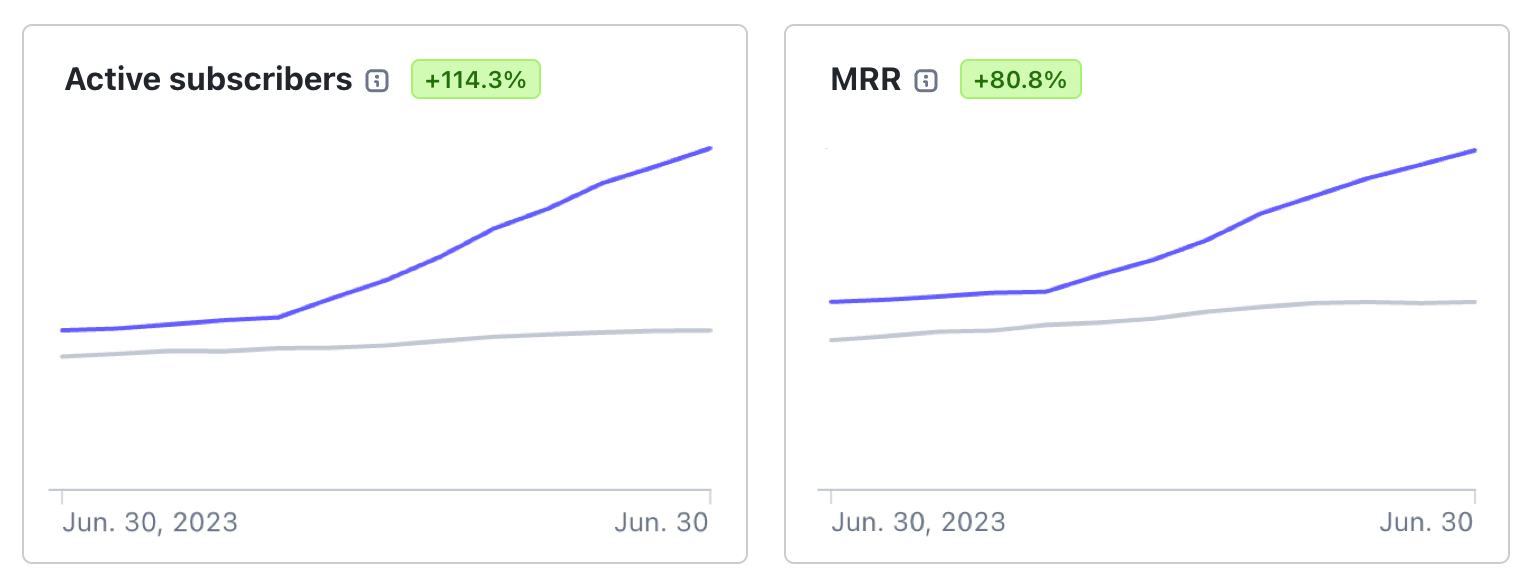

In the end, here’s what happened in the last year, compared to the previous year, as told through some key metrics.

Unsurprisingly, our average revenue per user went down compared to last period. Fortunately, our margins, being a SaaS company, are still fairly high, and our subscriber lifetime value is on an upward trend!

Our number of active subscribers (and by extension, our community size) shot up in the last 10 months, mostly thanks to word-of-mouth after news of the Mint shutdown. And with that, our MRR nearly doubled in the last 10 months.

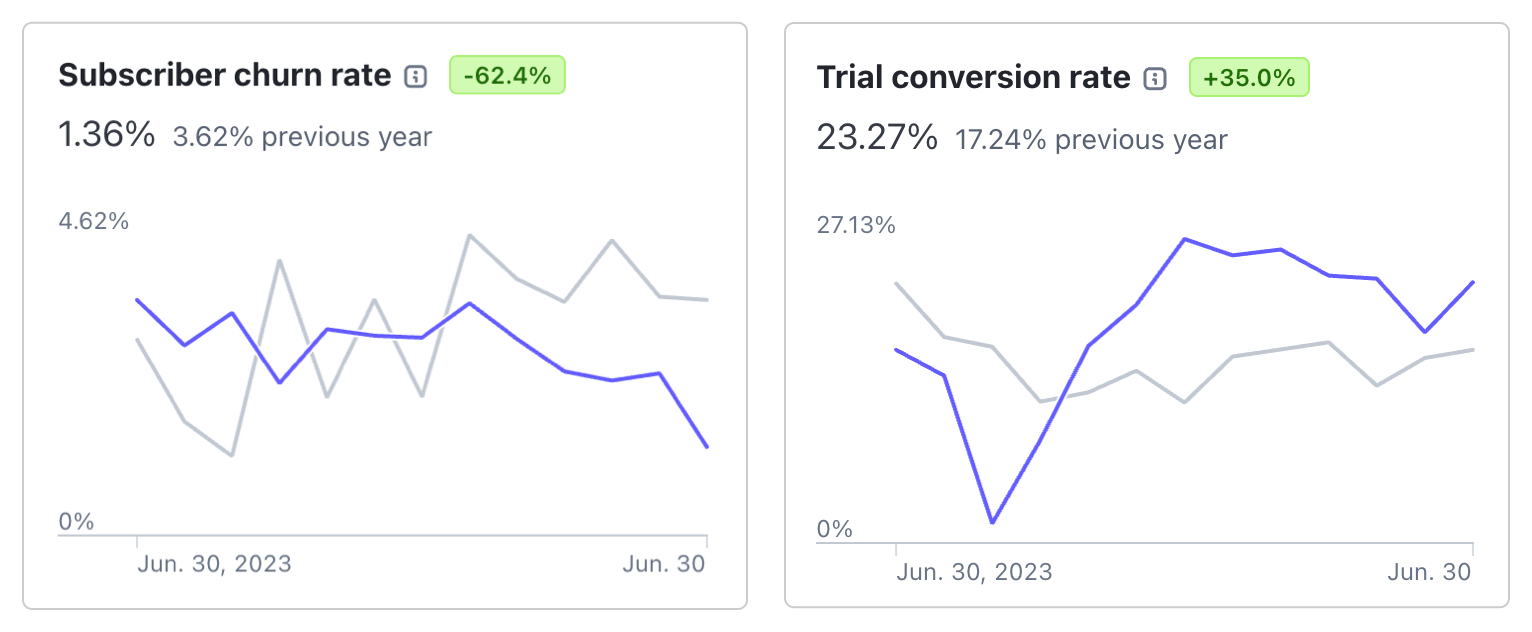

We’d been actively working on improving the product (as always) and re-investing more in the company, such as making some key hires. We also started offering users the option to pause their subscription and keep their data instead of canceling their subscription. As such, we have seen an impressive improvement in our churn and trial conversion rates.

In August 2023, we had an issue with a spammer creating thousands of new accounts which skewed our rates for the month. Unfortunately, it seems impossible to remove that data from Stripe, so we'll just have to live with that dip in the graph.

In conclusion, lowering our prices did not kill our business! In fact, I would say it helped do the opposite by priming us for even greater success after the Mint shutdown was announced.

Why were we able to do this?

Our ability to introduce this pricing change stems in part from our unique operational model:

1. We are web-first

Supporting both an Android and iOS app would require two separate engineering teams, in addition to our existing web team. Furthermore, by not being on the App Store or Play Store, we are not forced to share our revenue (15% to 30%!) with these giants.

For this reason, we are heavily investing in our developer ecosystem via our developer API. There are some awesome 3rd party Lunch Money apps available thanks to our developer community, such as Lunch Money Pal for iOS (currently available on TestFlight) and Lunch Money Companion for Android.

2. Lean team

At the time of writing, the Lunch Money team consists of 5 (excluding Jen!), all of whom are working with us on a part-time, contractor basis. While this is the case, our longest contractor has been with us for nearly 5 years! We’re lucky to work with this team because they all believe in the product and are in it for the long haul despite the unique working structure.

Everyone we hire is an expert in their field, self-sustainable and highly efficient even on a part-time basis. We have virtually no meetings and everything is done async on Discord. This allows us to move quickly to focus on building the best possible product.

3. Sustainability

Unlike many startups of a similar age, Lunch Money is a financially sustainable operation, and it has been for over half of our lifetime! Making the decision to lower pricing was a calculated risk which paid off – only 10% of legacy users switched their plans to a lower pricing point. About 37% of users on our new pricing plan pay above $100 annually (including those who choose to stay on the monthly $10 plan), and they account for over 60% of revenue generated. In the end, we feel our users want to see us succeed and are happy to pay a higher price than what’s expected of them. And for that, we’re so grateful!

What are you paying for?

When you subscribe to Lunch Money, you’re supporting a small, independent company. Here’s how your subscription helps us:

Active development: Your subscription directly funds the continuous development of Lunch Money. This includes paying for contractors, covering server costs, acquiring essential tools, and purchasing software— everything we need to keep the business running smoothly and our finances healthy.

Ad-free and honest experience: We charge a subscription fee to avoid relying on external income sources, such as advertisements, partnerships with financial institutions, solicitations to sign up for credit cards and loans, etc.

Our independence: We don’t have corporate shareholders or investors, so we never have to answer to external pressure to continuously increase our revenue streams. Our sustainable, profitable model means we’re here to stay, without the risk of sudden shutdowns that leave users scrambling for alternatives.

And most importantly… being 100% customer-funded fuels our passion to continuously make the Lunch Money experience delightful for everyone!

Conclusion

Being able to stand on our own two feet as a company allowed us to focus on what’s important to us: running a company we can truly be proud of and redefining what it means to gain control of your finances for our users.

Whether you choose to pay $40 or $100+, the collective Lunch Money community keeps us sustainable. And honestly, we love you all the same. Thank you for supporting us on this journey!